REPUTATION

REBOUND

Buoyed by its efforts to help consumers and businesses weather the pandemic, the banking industry saw its reputation improve for the first time in several years. Our annual survey offers some insight on how to keep the goodwill flowing.

By Matthew de Paula

When BOK Financial conducted a leadership audit as part of its succession planning process two years ago, some worrisome gaps emerged.

“It was skewed pretty significantly by age — 55 and older,” said Steven Bradshaw, president and chief executive of the $40 billion-asset BOK. “It doesn’t take much of a jump to realize that you’re going to have a pretty significant change in leadership over the next 10 years as you’re seeing people retire.”

The upper ranks also lacked diversity, in contrast to other levels of the organization, he said.

This exercise prompted BOK to create a diversity and inclusion council, which since its inception in 2019 has spearheaded changes in corporate policy and recruiting, including experimenting with artificial intelligence to reduce unconscious bias.

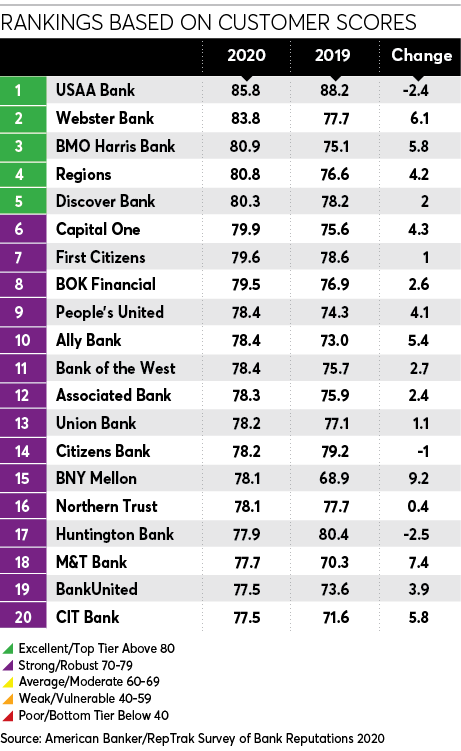

Such changes within the Tulsa, Okla., company also appear to have made a positive impression outside of it, based on the annual American Banker/RepTrak Survey of Bank Reputations. (The RepTrak Co. was formerly called the Reputation Institute.)

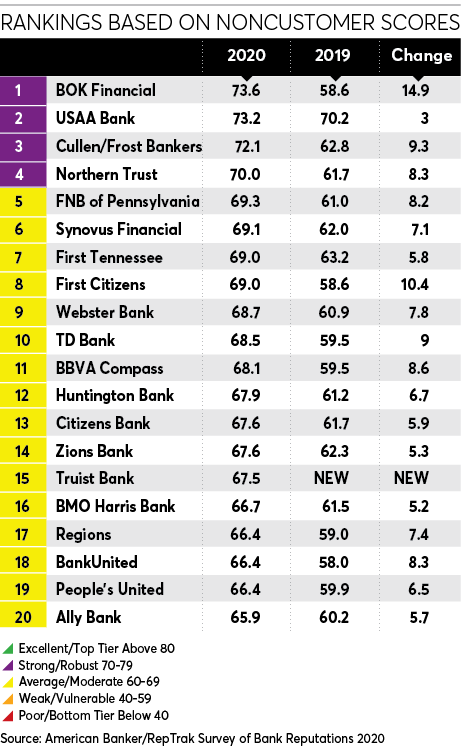

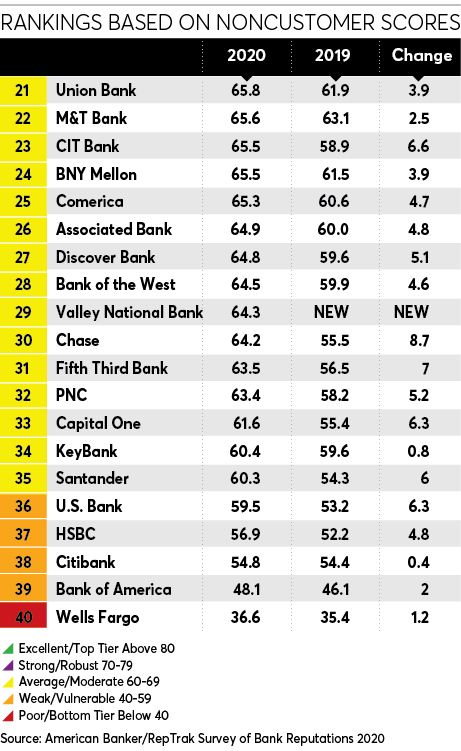

Of the 40 banks evaluated in the survey, BOK earned the highest rating in the workplace category among noncustomers familiar with it. BOK also ranked second with noncustomers in each of the six other categories the survey looks at: products and services, innovation, leadership, performance, citizenship and governance.

In a year when the banking industry’s reputation surged, BOK registered the biggest improvement of all the banks among noncustomers, vaulting to first place in that ranking, ahead of even USAA Bank, which had been at the top for two years running.

Bradshaw said one of the likely reasons BOK made such a favorable impression on noncustomers is that its employees have been especially visible during the pandemic in helping local nonprofits.

“I’m proud of that and proud of the industry, because I see a lot of banks stepping up to do that as well,” he said.

From villain to hero

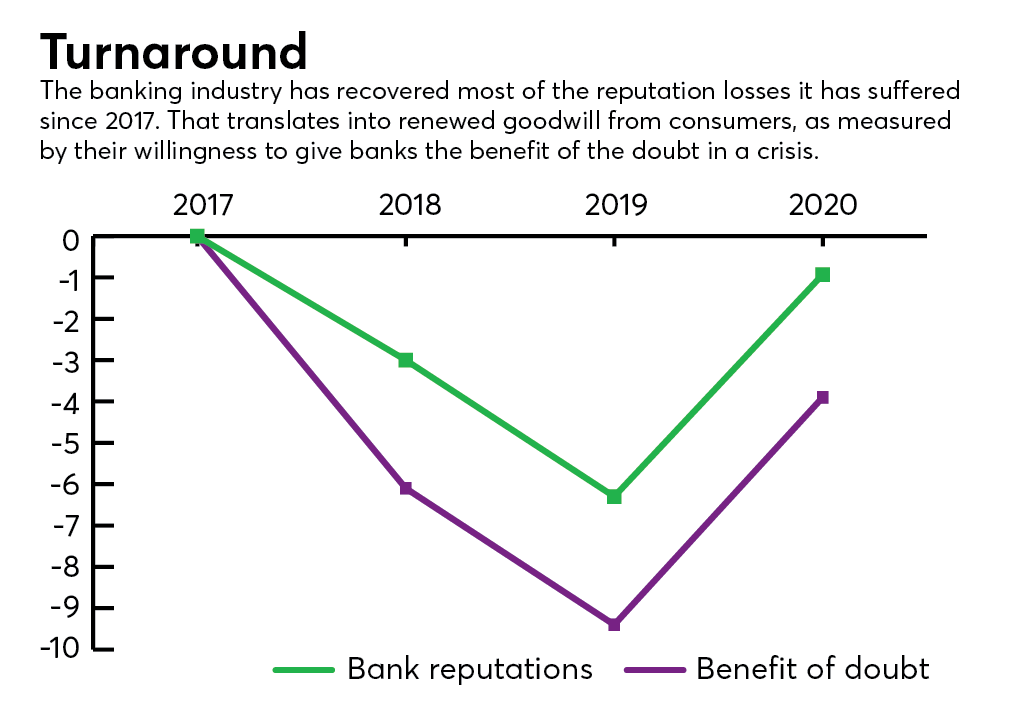

After dropping for the past two years, bank reputations are once again on the rise, thanks in large part to the goodwill banks have generated by helping customers and employees weather the pandemic.

In the survey conducted this spring, the banking industry as a whole scored a 68.6 out of a possible 100 — a 5.4-point improvement from last year.

“Not only is that statistically significant by a long shot, that’s a big move overall for an industry,” said Bradley Hecht, an executive vice president at RepTrak.

Though the score is still considered “average,” the industry regained nearly all of the ground it had lost since 2017, coming close to the 70-point mark that signifies a “strong” reputation.

With the pandemic battering the economy, and consumers and businesses suffering, banks have been thrust into the news more often than usual in recent months, mostly in positive ways.

Many consumers were allowed to temporarily skip payments on home and auto loans without it impacting their credit score. Many struggling small businesses received a lifeline in the form of Paycheck Protection Program loans. And many banks are increasing their philanthropic efforts to help community organizations like food banks keep up with demand.

The positivity that is being generated by such efforts stands in stark contrast to how people have reacted to the banking industry during previous crises, Hecht said.

Because banks have much more of a capital buffer to sustain them these days, the industry cast as the villain of the financial crisis has managed to play more of a hero this time — at least so far.

“It really is a fascinating intersection between a select few industries that historically were poorly perceived pivoting during the COVID crisis to not only do good things, but for once get credit for it without a lot of skepticism,” Hecht said.

Besides banking, Hecht cited the oft-maligned pharmaceutical industry — which is tasked with creating a vaccine for the novel coronavirus — as another benefactor of current consumer goodwill.

The upshot is that both banking and pharma have been able to “rewrite their reputations” as a result of the pandemic, Hecht said.

One of the benefits of that is people are more willing to give a bank the benefit of the doubt when something goes wrong.

A stronger reputation also translates into a greater willingness to do business with a bank and recommend it to others.

All three of those metrics have increased from last year, but the steepest improvement is with the benefit of the doubt, which means banks are regaining trust, Hecht said.

Gaining momentum

Banks are also benefiting from some momentum they started to create before the pandemic hit.

Many banks have taken note of how the public’s expectations on corporate citizenship and social activism are changing. Some executives are becoming more visible and vocal advocates for tackling issues like racial injustice, climate change and gender discrimination.

The survey offers some insight into how such factors influence perceptions of a bank, which in turn can help inform the strategy for improving a bank’s reputation.

“The bank that is perceived to have a higher purpose is much more reputable — that’s why it’s so important,” said Sven Klingemann, research director at RepTrak.

RepTrak has a new Purpose Power Index that helps companies track how well they are doing on that front, and it found a strong correlation between the purpose and reputation scores. The new index gauges consumer perceptions of companies on four criteria — having a purpose beyond just making a profit, being committed to changing the world for the better, doing things to benefit all stakeholders, not just shareholders, and helping people and communities.

BOK took the top spot with noncustomers in that new index and second place with customers.

Bradshaw said that, while having values and talking about them is important, the key to success is in what a company does to live those values, whether that entails actively pursuing greater diversity in the senior ranks or manning food banks.

“It’s more about actions than words,” he said.

He gives a lot of credit to employee-led community initiatives for generating positive sentiment for his company, saying more than 1,350 people from BOK logged nearly 34,000 volunteer hours last year.

“I think that shapes how people view us,” Bradshaw said. “That’s where they see us, that’s where they get a sense for what the values and the purpose of the company are, and frankly, it leads to more business for us.”

BOK’s community relations team helps organize the volunteer manpower around needs employees themselves identify in their communities, often with the backing of the BOK Foundation, which handles the company’s charitable giving. The corporate communications team helps get the message out, internally and externally.

One area of recent focus has been food insecurity. “We’ve done incremental giving and volunteering in that space because obviously there is a need that’s come out of the pandemic,” Bradshaw said.

Banking on purpose

Hecht noted several data points that reflect how consumer perceptions of whether a bank has a higher purpose is having greater influence on reputation scores.

Questions about “having a positive societal influence,” “equal workplace opportunities” and “environmental protection” were among those that increased the most in relative importance.

Having a positive societal impact alone saw “almost a 50% increase in relative importance from the prior year as a reputation driver” among customers, Hecht said. “That’s a big deal.”

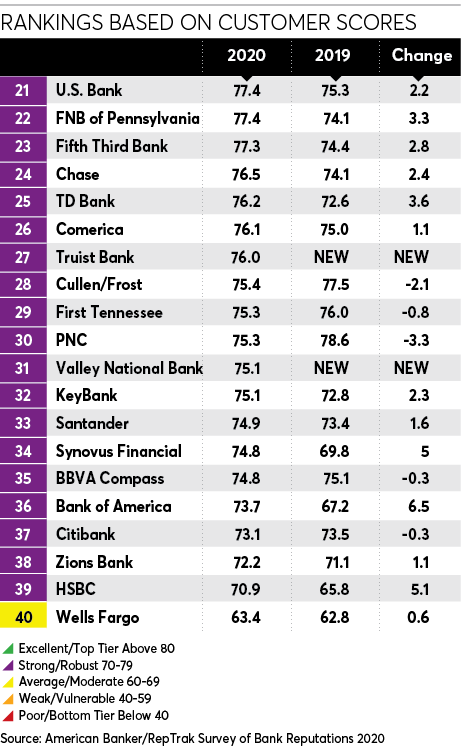

As for how banks are living up to expectations with regard to citizenship, both customers and noncustomers rate them higher this year than last. But regional banks as a group got the most credit for being good corporate citizens, with a 6.7-point increase in their citizenship score among noncustomers putting them at 66.8.

“That is a huge, huge change,” Hecht said. “That is gigantic, relatively speaking.”

The citizenship score improved by 5.1 points, to 68, for nontraditional banks, a group that includes online players like Ally and Discover, and by just 1.3 points, to 51.8, for large banks.

Citizenship is among the top three drivers of reputation for both customers and noncustomers this year, as is governance, which, in this case, is a gauge of whether people perceive the bank as fair, ethical and transparent. Products and services rounds out the top three in importance.

“It might be the first time in a while that the top three were the same for customers and noncustomers,” Hecht said.

Innovation counts

Perhaps because the pandemic is forcing more people to interact with their banks through digital channels, innovation is another reputation driver that has become more important.

Questions about whether a bank “adapts quickly to change” and whether consumers consider it an “innovative company” jumped in relative importance.

At BOK, which had the second-highest innovation score among noncustomers, the biggest jump in digital adoption this year hasn’t been in retail banking — that segment has been going digital for years now, Bradshaw said — but rather on the commercial and wealth management sides of the business.

“We’re a very large organization in terms of wealth management — it’s more than a third of the total revenue of the bank — and that’s a group that has largely been very focused on face-to-face business in order to manage it,” Bradshaw said. “That’s also true for a lot of our larger corporate relationships.”

Capabilities BOK has built up over the past five years that might’ve been overlooked by high-net-worth and commercial banking clients before the pandemic are getting a lot more use now, he said. Some areas of the private wealth management and retail brokerage business experienced “upwards of a 65% increase” in logins from February to March.

“The other thing is we were quick to adopt virtual meetings and virtual forums for our clients,” Bradshaw said. “We did an awful lot of investment briefings, economic briefings and other things facilitated by our corporate communications group.”

He expects an increase in virtual interactions across all business lines to be a lasting outcome of the pandemic.

The way to win hearts

Besides fostering close ties to their communities, banks would do well to focus on developing a more positive and inclusive workplace environment.

The reputation survey shows that consumers increasingly care about how banks treat their employees.

Workplace gained importance as a driver of reputation across the board for every bank type, with customers and noncustomers alike.

Webster Bank scored high enough in the workplace category to rank second of all 40 banks among customers, after USAA. It was also one of only two banks to earn an “excellent” score from customers in the governance category, USAA being the other one. And it got the highest score among customers on the Purpose Power Index.

Chris Motl, the head of commercial banking for the $30 billion-asset Webster, said its strong culture of caring is the basis for how the bank treats both customers and employees.

“I narrow it down to, literally, we do the right thing,” he said.

The five core values it wants employees to embody are codified in “The Webster Way,” which have been printed on the back of everyone’s business cards for as long as he’s worked at the company, which is 16 years, Motl said. One of these mantras is, “We respect the dignity of every individual,” while others speak to a higher purpose, such as earning trust through ethical behavior and giving back to the communities the bank serves.

No matter how it’s defined, there’s something about the culture that resonates with people who stay, Motl said. Those who aren’t on board with it “eventually self-select out,” he said. “I’m glad I fit in the culture, because I think it sort of says something about me too.”

Like BOK, Webster also has made diversity and inclusion a focus.

This is an area that carries more weight with consumers lately. Such topics are top of mind since they have gotten broad media attention via social movements — starting a few years ago with #MeToo sexual harassment scandals in many industries and more recently amid the widespread protests over racial injustice after a Minneapolis police officer killed George Floyd by kneeling on his neck for more than eight minutes while he was handcuffed on the ground.

Based on the survey data, three of the biggest reputation risks for banks involve social justice: unequal pay by gender, unequal opportunities by race, gender or other factors, and discriminatory business practices.

“If you don’t pay people well, if you don’t give them equal opportunity, and you discriminate against them in your business, then that’s the trifecta of badness when it comes to risk for banks,” Hecht said.

BOK’s diversity and inclusion council, formed in April 2019, is led by Bradshaw himself, and one of the goals is to diversify its largely white, middle-aged, male leadership.

“I think over the next decade or so, as we see the accelerated retirement of the baby boomers, there’s going to be an even greater war for talent,” which will make the ability to attract top-notch people a major differentiator for banks, Bradshaw said. “One of the ways you win that war is to make sure that you’re building an organization that appeals as broadly as it can across every type of measurable demographic so that you have a chance at the best of the best.”

As part of that effort, BOK just rolled out unconscious-bias training for its leadership and those with hiring oversight. It also revamped the training for recruiters to make sure they get diversity and inclusion accreditation. And job descriptions are being updated to remove gender bias and “extreme modifiers,” while university recruitment and internship programs have an increased focus on women and minorities.

“We’re not the kind of company that says, ‘I’m sure it will happen naturally,’ ” Bradshaw said.

“Our message to ourselves was, ‘What can we do to accelerate that and make sure that we see a more diverse transition as we see leadership turnover in the company?’ ”

CEOs, listen up

That sort of leadership is crucial, the reputation survey indicates.

“CEOs are taking on a more important role,” said Klingemann, the RepTrak research director. “They’re testifying in front of Congress. There’s a political void and they’re sort of jumping in when it comes to talking about socioeconomic issues or inequality. There is this demand now to know what the bank stands for and I think CEOs have been forced to step up.”

RepTrak has started measuring consumer perceptions of CEOs, and it has found that for every point a CEO’s rating improves, a company’s overall reputation score has a corresponding increase of half a point, according to Klingemann.

This illustrates the importance of the CEO’s own reputation in either damaging or elevating the bank’s reputation overall, he said.

To help lift a bank’s reputation, CEOs should exercise their influence for the greater good, especially during a crisis like the pandemic, where all constituents, inside and outside of banks, are experiencing such a profound impact, he said.

Of the four drivers measured to evaluate CEO reputations — influence, leadership, management and responsibility — the importance of influence increased the most this year.

What that means is, “he or she needs to be able to make a difference,” Klingemann said.