On-Chain Finance

How blockchain infrastructure is reshaping institutional finance

American Banker's coverage of on-chain finance tracks how blockchain technology is being applied to real-world financial systems — not as a parallel ecosystem, but as a foundation for modernizing how assets move, settle, and are managed across institutions.

As banks pilot tokenized treasuries, smart contract-driven workflows, and real-time settlement tools, the conversation is shifting from innovation theory to infrastructure strategy.

While most applications remain in pilot phases, the shift toward programmable, blockchain-based systems is accelerating. American Banker tracks how financial firms are engaging with on-chain infrastructure — from tokenized treasuries and deposits to the emerging standards shaping the next generation of financial rails.

-

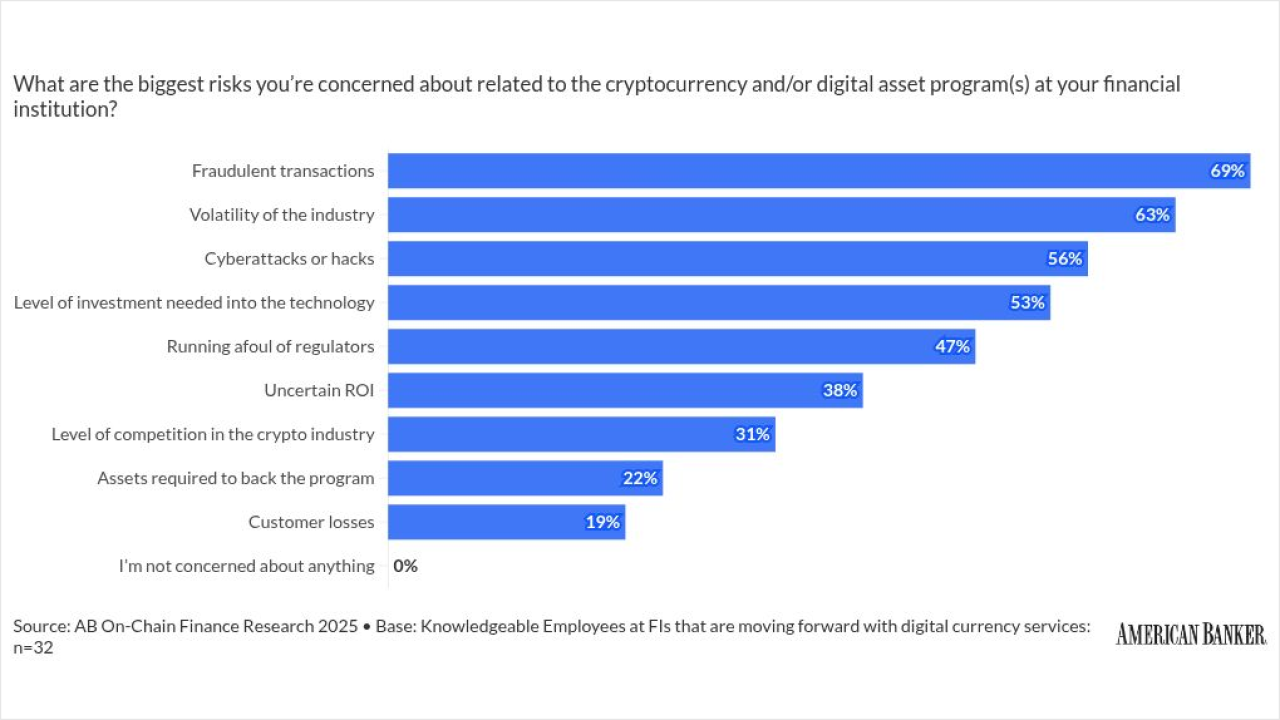

Digital currency can be tracked and if stolen "burned," then reminted and given back to its rightful owners. That could be a powerful anti-fraud tool.

July 30

July 30

-

The Securities and Exchange Commission agreed to pay $150,000 to crypto exchange Coinbase to settle a Freedom of Information Act lawsuit filed by the company two years earlier.

July 23

July 23

-

Draft cryptocurrency market structure legislation published Wednesday includes an ethics agreement that falls short of what Senate Democrats want and stablecoin yield language that banks have already disavowed.

July 22

July 22

-

"Ultimately, adoption and embedding in a company is going to be the differentiator for many firms on whether or not they're successful with AI," said BNY CEO Robin Vince.

July 15

July 15

-

The banks now let institutional clients mint and redeem Circle's USDC directly, turning them into stablecoin infrastructure providers.

July 9

July 9

-

With Robinhood Chain now live, the company is pushing into tokenized equities, stablecoin lending and international markets.

July 7

-

The Museum of American Finance opened a free, Smithsonian-affiliated home in Boston's Seaport on Friday, betting it can make money history stick.

July 2

-

The use of cryptocurrency products will only go truly mainstream when everyday consumers feel confident that their assets are not at risk of disappearing because of a mistake or an oversight.

-

Crypto firms are becoming the kinds of trusted third parties bitcoin was created to get around, raising the question of what digital currencies are even for.

-

The 21st century financial system that digital currency promised is being built, but by banks, not by the bitcoin crowd.

The first three months of the year coincide with the start of President Donald Trump's second term in office. Investors are likely to be more interested in banks' outlooks amid swings in tariff policy than the first-quarter results.

Frequently Asked Questions:

What’s driving adoption of on-chain finance among regulated institutions?

Rising demand for intraday liquidity, cost reductions in settlement, and automation of high-friction processes are pushing institutions to test blockchain-based infrastructure. On-chain finance offers a path to 24/7 operations, programmable compliance, and faster execution.

Banks are piloting tokenized assets, smart contract-driven workflows, and real-time settlement systems to replace or enhance legacy infrastructure. American Banker tracks how these shifts are unfolding across custody, payments, and capital markets — and what they mean for long-term competitiveness and regulatory alignment.

How is blockchain being used with on-chain finance?

Banks and other financial institutions are using blockchain as the foundation for on-chain finance, applying it to functions like settlement, payments, and asset custody. By moving assets — such as U.S. Treasuries or commercial deposits — onto blockchain-based systems, firms can track and transfer them more efficiently.

Some are using smart contracts to automate collateral movements or streamline post-trade processing. Others are testing blockchain for real-time cross-border payments and liquidity management. The goal isn’t to replace the financial system, but to update its core infrastructure with faster, more transparent, and programmable tools.

- Tokenized collateral for repo and derivatives markets

- Smart contract-based settlement and clearing

- Interbank payment networks using tokenized liabilities

What is the future of blockchain development?

Most are early-stage or permissioned pilots, but momentum is building. The future of blockchain development is moving toward more practical, behind-the-scenes uses — especially in finance. Instead of focusing on consumer-facing crypto projects, developers are working with banks, payment companies, and regulators to build systems that improve how money and assets move.

That includes things like faster settlement, tokenized deposits, and automated compliance tools. As the technology matures, the focus is shifting to reliability, interoperability, and fitting into existing financial infrastructure. Over time, blockchain may become less visible — but more essential to how financial systems operate.

What’s the current regulatory posture toward on-chain financial systems?

Cautious but increasingly engaged. Regulators are focused on legal finality, risk exposure, data integrity, and systemic impact. While public blockchains raise compliance flags, private or hybrid systems are receiving more favorable consideration in early guidance.How does on-chain finance intersect with stablecoins, tokenized deposits, and CBDCs?

On-chain finance is the infrastructure layer. Stablecoins and tokenized deposits are assets that live on top of it. CBDCs could integrate with or compete against these systems, depending on how central banks design interoperability and access.Who are the key players shaping the on-chain finance space?

A growing group of banks, asset managers, infrastructure providers, and fintechs are testing and deploying blockchain-based systems to modernize how financial assets are issued, moved, and settled.- JPMorgan Onyx: tokenized collateral and payments

- BNY: custody for digital assets

- Citi: institutional DLT architecture

What are the latest on-chain finance trends and latest news?

Our reporting tracks regulatory moves, pilot expansions, major partnerships, and infrastructure shifts as they happen. Follow our on-chain finance coverage for real-time insight into what’s next.- Tokenized deposits are gaining real traction

Major banks—including JPMorgan and Citigroup—are piloting deposit token services to enable real-time liquidity, cross-border payments, and automated collateral flows. Citi's blockchain‑based deposit token system, for example, enables institutional clients to settle payments and manage trade finance around the clock on Ethereum‑based rails - Banks are integrating with public blockchains

Projects like JPMorgan’s “Project Guardian” involve tokenized bonds and deposits circulating on public blockchains, with banks functioning as trust nodes. The aim: combine public‑chain transparency with institutional control.