-

Lawmakers and regulators opted to delay compliance for banks that have implemented the credit loss standard, sparing them near-term capital hits.

March 27

-

The $2 trillion stimulus package, which the House passed earlier in the day, aims to expand Federal Reserve liquidity resources and provide financial institutions with some regulatory relief.

March 27

-

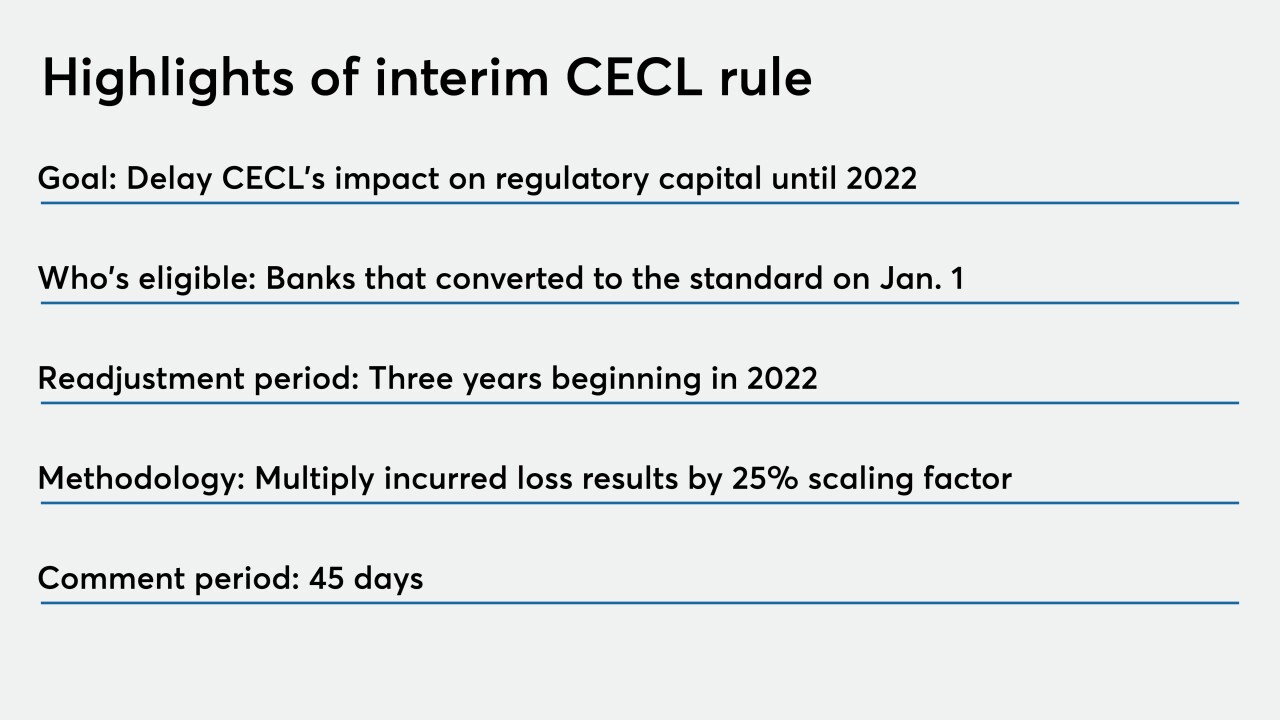

Regulators are allowing banks that implemented the loan-loss standard to forestall any capital hits until 2022.

March 27

-

NAFCU and CUNA wrote to the regulator asking for a variety of measures to help credit unions weather the pandemic, including not implementing the CECL standard until at least 2024.

March 26

-

Details of the $2 trillion deal were still fluid Wednesday, but lawmakers were closing in on a plan that would aim to put lenders and consumers alike on stronger financial footing as they weather the coronavirus pandemic.

March 25

-

Policymakers should abolish the new accounting standard because it could distract banks at exactly the moment they need to be focused on pulling their communities from the brink of recession.

March 25 Signature Bank of New York

Signature Bank of New York -

The $2 trillion deal passed by the Senate late Wednesday would aim to put banks and consumers alike on stronger financial footing as they weather the coronavirus pandemic.

March 25 -

If the new accounting standard poses too many risks during an economic crisis, then it's probably not a good idea at all.

March 24

-

Congressional proposals could expand Federal Reserve liquidity support, delay a new credit loss accounting standard, provide certain accounts with unlimited deposit insurance and more to help businesses and consumers reeling from the coronavirus outbreak.

March 23

-

The FDIC's call for FASB to postpone the loan-loss accounting standard's effective date could put pressure on other agencies to follow suit.

March 20

-

Some banks have closed branches or restricted access and bank tech resources are being overwhelmed; bank pays a record SKr4 billion ($400 million) for issues.

March 20

-

FDIC Chairman Jelena McWilliams, citing concerns about the coronavirus outbreak, is the first regulatory chief to call for suspending the accounting standard for expected loan losses.

March 19

-

The FDIC chairman, citing concerns about the coronavirus outbreak, is the first regulatory chief to call for suspending the accounting standard for expected loan losses.

March 19 -

The Consumer Financial Protection Bureau will have a busy week starting with Director Kathy Kraninger testifying before lawmakers on Tuesday.

March 9

-

Rep. Blaine Luetkemeyer, R-Mo., said Congress has "got to be pushing back" against the Current Expected Credit Losses standard, while Rep. Steve Stivers, R-Ohio, indicated that not all Republicans view the cannabis banking issue the same way.

February 26

-

At a credit union conference, Rep. Blaine Luetkemeyer, R-Mo., said Congress has "got to be pushing back" against the Current Expected Credit Losses standard, while Rep. Steve Stivers, R-Ohio, indicated that not all Republicans view the cannabis banking issue the same way.

February 26 -

The credit union regulator's portfolio sale dashed the hopes of a group of New York taxi drivers looking for relief.

February 20

-

Congress should further expand a tiered regulatory system to help community banks better serve local neighborhoods.

February 13

-

Bank will have more business lines, all reporting to the CEO; a research paper says the accounting rule could result in eased capital rules.

February 12

-

M&T hires Aarthi Murali away from JPMorgan Chase as its customer experience chief; when a small town loses its only bank; why more banks are ditching their legacy core vendors; and more from this week’s most-read stories.

February 7