Community banking

Community banking

- Washington

Middle Atlantic community banks that need correspondent banking services have no shortage of options; there are bankers’ banks based in Maryland, Pennsylvania, and Virginia, and the nation’s largest bank for other banks opened a Maryland office two years ago, mainly to help small banks make loans that exceed their limits.

November 12 - Pennsylvania

F.N.B. Corp. in Hermitage, Pa., has been anxious to expand beyond its Rust Belt markets, and on Friday it struck a deal that would move it into some of the faster-growing regions of its home state.

November 12 -

Ooh! Nothing like waking up to a disagreeable American Banker story ["Banks, CUs to Fill Payday Gap? Maybe," Nov. 7]. Hard way to start off your day! Creates about the same visceral sensation as dropping a really hot cup of coffee in your lap during the morning commute!

November 12 - Virginia

The clock is ticking on an Alexandria, Va., company formed last year for the purpose of buying banks.

November 12 -

Maryland

MarylandIt has been a challenging year for community banking companies, but most can take comfort at least in the fact that they have little or no exposure to subprime mortgages.

November 9 - Tennessee

Tennessee Commerce Bancorp Inc. in Franklin said Thursday that issues surrounding a compensation committee vote removed the danger of its being delisted from the Nasdaq Stock Market.

November 9 -

To the Editor:

November 9 - Florida

Shares of Sun American Bancorp continue to tumble amid speculation about further deteriorating credit quality at the Boca Raton, Fla. banking company.

November 9 -

- Colorado

The Credit Union Journal

November 8 -

Texas

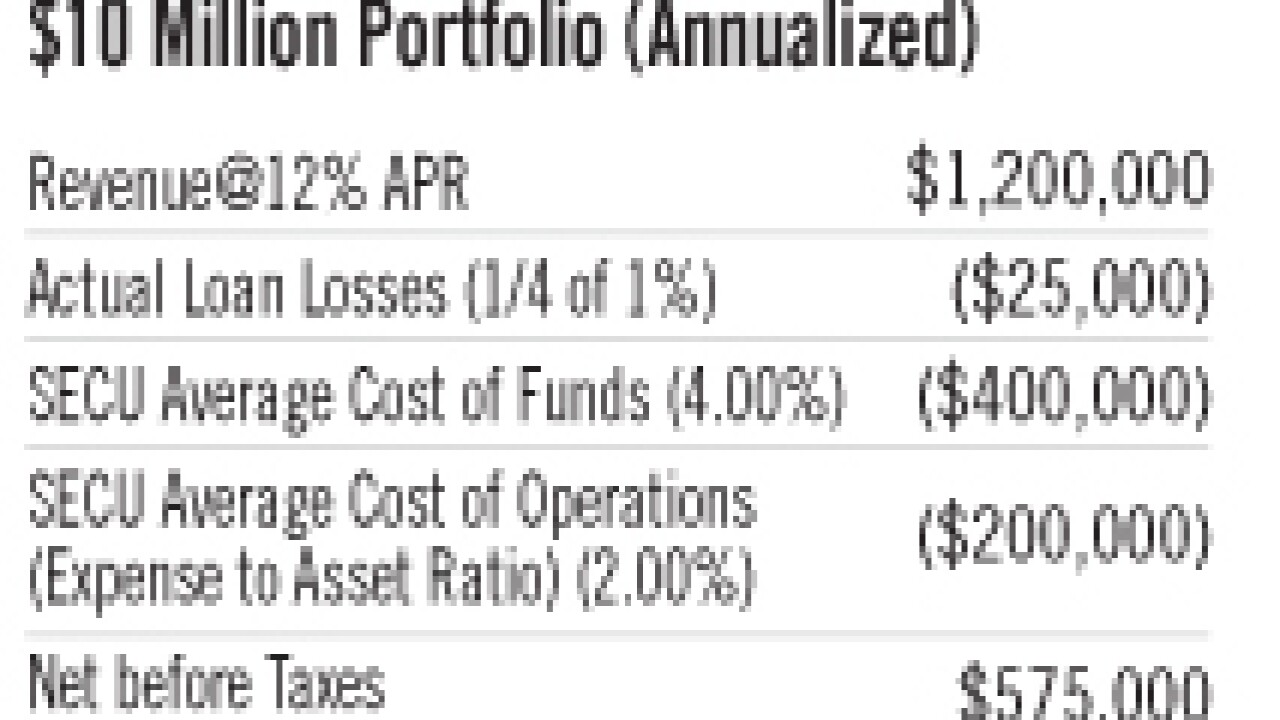

TexasPayday lending is on the verge of being outlawed in the District of Columbia, but the fact remains that consumers will still need access to short-term, emergency loans. Credit unions already are marketing what they call lower-cost alternatives to the traditional payday loans, and consumer finance firms offer products that could be attractive to consumers who have used payday lenders. Even bankers, with a nudge from the Federal Deposit Insurance Corp., might consider getting in on the action. The D.C. City Council passed the Payday Loan Consumer Protection Act of 2007 in September, and Mayor Adrian Fenty, a Democrat, signed it last month. The bill, which would cap the annual percentage rate on payday loans at 24%, is in Congress’ hands now. If approved, it would likely go into effect by Jan. 8. Payday lenders have said the caps would make it impossible for them to make loans profitably and likely would force them to stop lending in Washington. Ultimately, they argue, consumers would suffer, because they would have fewer options for short-term, small-dollar loans. But Mary Cheh, the city councilwoman who sponsored the legislation, said in interview with American Banker shortly before the bill was passed that she was confident “the void will be filled” by the likes of finance companies and credit unions. The District of Columbia would join 13 other jurisdictions that have either banned payday lending or capped rates on the loans, essentially forcing payday lenders out. North Carolina was one of the first to ban it, in 2001, though for years many lenders were able to get around the law by entering rent-a-charter agreements with out-of-state banks. It took Attorney General Roy Cooper five years of investigations and lawsuits — not to mention a crackdown on charter renting by federal regulators — to force out all of the state’s payday lenders. Sharon Reuss, a spokeswoman for the Center for Responsible Lending, a consumer watchdog group in Durham, N.C., said the disappearance of payday lenders has saved the state’s residents $150 million a year in fees and interest payments. Alternative loan products, specifically the State Employees Credit Union Salary Advance Loan, have emerged to meet residents’ need for emergency cash, she said. The credit union began exploring small-dollar loans after an August 2000 survey found that many of its members, made up of state and public school employees and their families, had been borrowing from payday lenders. Most could not qualify for conventional loans, because of spotty credit reports and high debt-to-income ratios. “We were trying to figure out why in the world our members were using payday lenders,” said Leigh Brady, the credit union’s senior vice president of education services. “We needed something to get them away from the payday lenders.” A program the credit union began in 2001 lets members take out salary advance loans with a maximum of $500, a minimum of $50, an APR below 18%, and no fees. Every time a loan is granted, 5% of the advance is deposited into a cash account and accumulates interest at the passbook rate. The money is used to securitize the loan, as well as to encourage members to save. “The savings is the best feature of the whole program, because it helps to break the cycle of debt,” Ms. Brady said. Currently, 50,000 members of the credit union use the program. A typical payday lender charges a fee of $15 for every $100 borrowed, but the interest on a $500 salary-advance loan from SECU is $5. The Community Financial Services Association, a trade group for payday lenders, said credit unions cannot make small-dollar loans profitably. “Some credit unions and good will industries are offering payday advances and charging $10 per $100 and losing money,” said Steven Schlein, a spokesman for the group. “It’s not working for them, because the right price for a payday loan is between $15 and $17.” Credit unions “don’t have to pay taxes because they are nonprofit, but they still can’t get away with going that low.” There are 49 payday-lending outlets in Washington, and it is likely that some, if not all, would pull up stakes when the rate caps take effect. In anticipation of that, a coalition of credit unions is marketing Stretch Pay, a $250 or $500 revolving line of credit for which borrowers pay an annual fee of $35 or $70. Customers must repay the loan within 30 days before another advance can be taken. “Credit unions have always been the best option for consumers to get loans, because of their low rates,” said Jennifer Gore, the chief advocacy officer for the Maryland and D.C. Credit Union Association. “At credit unions, we believe that consumers should end up better off, rather than worse off, after getting a loan.” Yasuko Fumoro, a spokeswoman for Microfinance International Corp., a Washington consumer lender that targets the unbanked or the underbanked, particularly Hispanic immigrants, said it offers a consumer product that could be an option for the city’s residents. The loan carries an interest rate of 24% and ranges in size from $500 to $3,000. The biggest difference between its loans and payday loans is that consumers repay them in installments, as they would car or home loans, Ms. Fumoro said. Banks that are based in or do business in Washington could also step in, with encouragement from regulators. The FDIC is taking applications for its Small Dollar Loan program, a two-year test to encourage banks of all sizes to offer payday loan alternatives. So far the FDIC is talking to 57 banks, with $40 million to more than $100 billion of assets, and a Washington bank could very well join that group.

November 7 - New Jersey

Clifton Savings Bancorp Inc. in New Jersey said that three of the four claims of corporate waste brought against it in 2004 by the activist shareholder Lawrence Seidman have been dismissed.

November 7 -

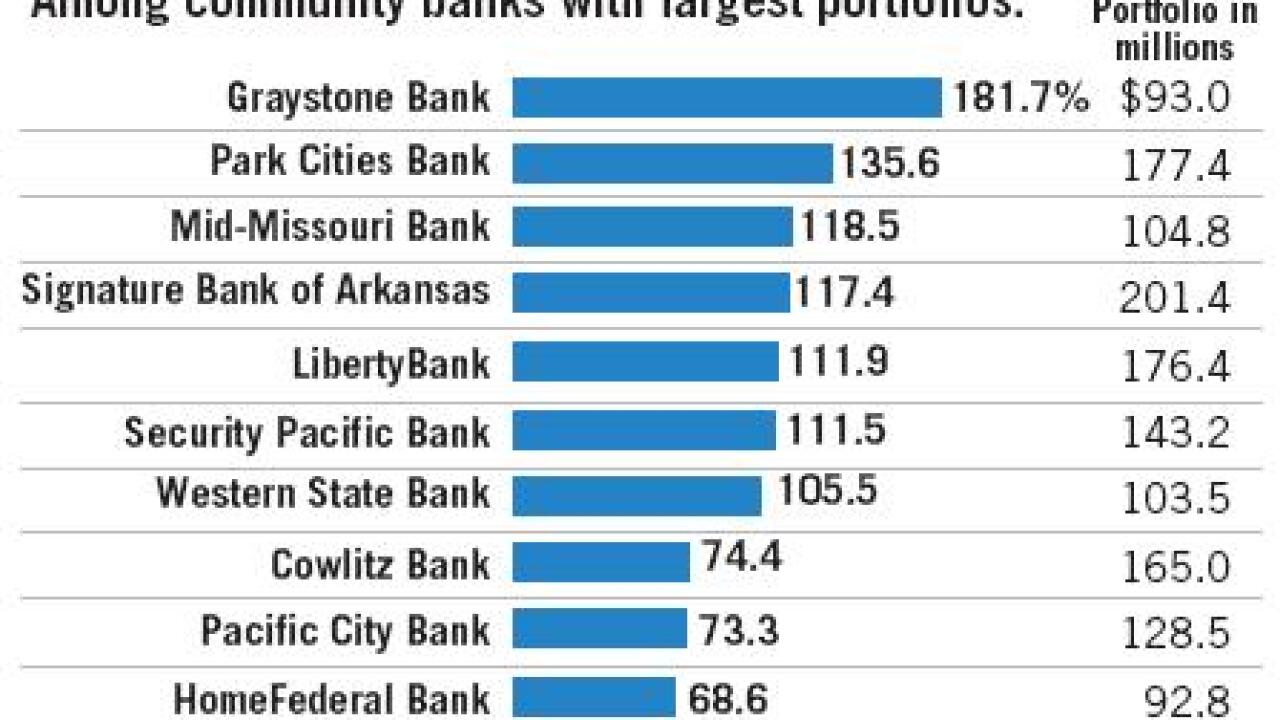

(Click here to see the top 150 community banks ranked by C&I loan portfolios, as of June 30, 2007.)

November 7 - Texas

Its coffers full with freshly raised cash and its first acquisition out of the way, the bank holding company CBFH Inc. in Beaumont, Tex., is scouting for more deals.

November 6 - California

A California credit union has become the latest casualty of the meltdown in the housing markets.

November 6 - Massachusetts

Youthful enthusiasm and fresh ideas.

November 6 - Massachusetts

First Ipswich Bancorp in Massachusetts said Monday that it narrowed its third-quarter net loss to $386,000, from $626,000 a year earlier.

November 6 - California

Pacific Mercantile Bancorp Inc. in Costa Mesa, Calif., said Friday that its third-quarter earnings fell nearly 18% from a year earlier, to $1.4 million.

November 5 - New York

Sterling Bancorp in New York reported a third-quarter profit of $3.1 million, or 17 cents a share, compared with a loss of $4.4 million, or 23 cents a share, a year earlier.

November 5