Kate Berry has covered the Consumer Financial Protection Bureau for American Banker since 2016. She joined the publication in 2006 covering mortgage lending and the financial crisis. Berry also has covered big banks including Bank of America, J.P. Morgan Chase and Wells Fargo. She has won five awards from the Society of American Business Writers and Editors, and has worked at several news organizations including the Orange County Register, the Los Angeles Business Journal and the Associated Press. Berry began her career as a clerk at the New York Times.

-

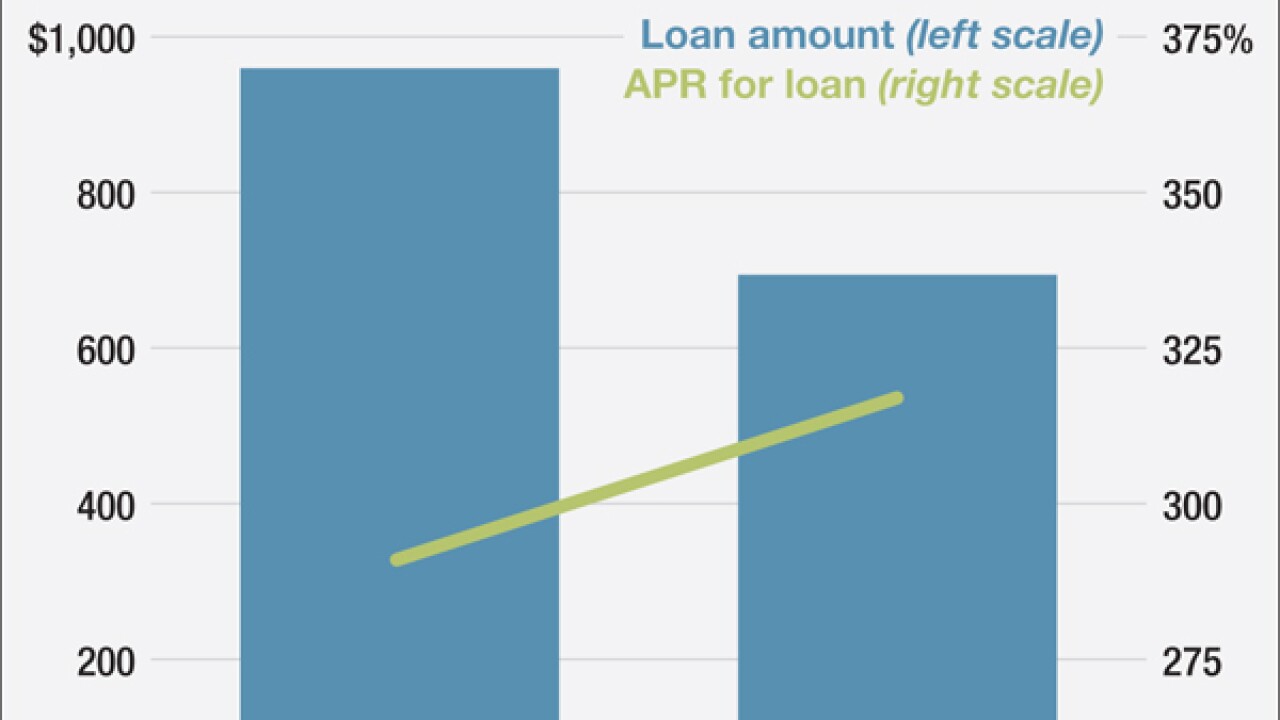

Lenders are questioning the legal justification for the Consumer Financial Protection Bureau's putting a 36% annual percentage rate threshold in its payday proposal, claiming loans made at that rate are unprofitable. That figure has been the subject of intense debate in the past decade.

June 8 -

The Consumer Financial Protection Bureau's complex payday lending proposal is sparking concerns that state legislatures will try to repeal existing usury laws and allow a parade of pro-payday-lending bills to move forward.

June 7 -

The Consumer Financial Protection Bureau filed a lawsuit Monday against payment processer Intercept Corp. and its two top executives for allegedly enabling clients to withdraw millions of dollars' worth of illegal charges from consumer bank accounts.

June 6 -

The Consumer Financial Protection Bureau filed a lawsuit Monday against payment processer Intercept Corp. and its two top executives for allegedly enabling clients to withdraw millions of dollars worth of illegal charges from consumer bank accounts.

June 6 -

The Consumer Financial Protection Bureau's complex payday lending proposal is sparking concerns that state legislatures will try to repeal existing usury laws and allow a parade of pro-payday-lending bills to move forward.

June 2 -

Although the Consumer Financial Protection Bureaus long-awaited proposal to establish the first federal rules for payday, auto title and high-cost installment loans offers a nod to NCUAs Payday Alternative Loans (PALs) program, CUs are concerned the plan will stifle their ability to offer consumer-friendly alternatives to an often predatory market.

June 2 -

The Consumer Financial Protection Bureau's long-awaited proposal to establish the first federal rules for payday, auto title and high-cost installment loans did not include a provision that banks had planned would allow them to compete by offering small-dollar installment loans.

June 2 -

The Consumer Financial Protection Bureau will unveil sweeping federal regulations Thursday for payday lenders that could open the door for competition from banks, while forcing lenders to move toward longer-term installment loans. Here's what to track when the plan is released.

May 31 -

The Consumer Financial Protection Bureau will unveil sweeping federal regulations Thursday for payday lenders that could open the door for competition from banks, while forcing lenders to move toward longer-term installment loans. Here's what to track when the plan is released.

May 31 -

Academics are challenging the Consumer Financial Protection Bureau's study of auto title loans, calling the findings inconsistent with state data. The study found that one in five borrowers who take out a short-term auto title loan end up having their vehicle repossessed. Some states report vehicle repossessions rates of between 6% and 11%.

May 26 -

The Consumer Financial Protection Bureau is making an end run around existing regulations to collect new data on overdraft programs, the American Bankers Association claims.

May 23 -

The agency posted its semiannual rulemaking agenda

on a blog late Wednesday updating the next steps it will take on several areas of rulemaking. The CFPB expects to issue rules for prepaid reloadable cards, mortgage servicing and mortgage disclosures this summer but set no specific deadlines yet on overdraft and debt collection.May 19 -

The agency posted its semiannual rulemaking agenda

on a blog late Wednesday updating the next steps it will take on several areas of rulemaking. The CFPB expects to issue rules for prepaid reloadable cards, mortgage servicing and mortgage disclosures this summer but set no specific deadlines yet on overdraft and debt collection.May 19 -

The bureau said Wednesday that it plans to hold a public hearing in Kansas City, Mo., to discuss small dollar lending. The hearing will be held at the Kansas City Convention Center and will feature remarks from CFPB Director Richard Cordray, as well as testimony from consumer groups, industry representatives, and the public.

May 19 -

The bureau said Wednesday that it plans to hold a public hearing in Kansas City, Mo., to discuss small-dollar lending. The hearing will be held at the Kansas City Convention Center and will feature remarks from CFPB Director Richard Cordray, as well as testimony from consumer groups, industry representatives and the public.

May 18 -

The Consumer Financial Protection Bureau's proposal to limit the use of arbitration clauses came under attack Wednesday for potentially raising costs and liability for financial firms.

May 18 -

The Consumer Financial Protection Bureau's proposal to restrict the use of arbitration clauses would allow it to seize enormous amounts of data from financial firms that could lead to more enforcement actions, according to industry lawyers.

May 18 -

The Consumer Financial Protection Bureau's proposal to restrict the use of arbitration clauses would allow it to seize enormous amounts of data from financial firms that could lead to more enforcement actions, according to industry lawyers.

May 18 -

The Consumer Financial Protection Bureau found that one in five borrowers who take out short-term auto title loans have their vehicle seized for failing to repay the loan.

May 18 -

The Supreme Court on Monday ruled that private attorneys hired by states are not in violation of the Fair Debt Collection Practices Act when using official letterhead to collect a debt. The case has been watched closely by financial institutions for its interpretation of false, deceptive or misleading practices.

May 16