-

SANTA FE, N.M. – NCUA said last night it liquidated Land of Enchantment FCU and assigned the member accounts of the one-time $11 million credit union to Guadalupe CU, a $102 million credit union also in Santa Fe. Land of Enchantment lad losses of $765,000 for 2009 and of $297,000 for 2010 and net worth of just 1% at year-end 2010. The credit union, the fifth failure of 2011, was chartered in 1951 to serve the employees of the New Mexico Department of Public Welfare.

March 7 -

WARNER ROBINS, Ga.-Numerous business practices are responsible for Robins FCU's 1.49% ROA in 2010-including new technology, employee training, and net interest margin management. Yet the credit union says one simple business philosophy has made the biggest contribution.

March 7

-

ALEXANDRIA, Va.-Credit union net income was up 208% during Q4 2010, according to NCUA data released last week, although credit union membership actually declined during the quarter.

March 7

-

OGEMA, Wis. – NCUA and state regulators took over and liquidated tiny Wisconsin Heights CU this afternoon and assigned the member accounts of the fourth credit union failure of 2011 to CoVantage CU, the $860 million credit union based in nearby Antigo. Wisconsin Heights has just 501 members and $713,000 in assets at liquidation and never reached $1 million in assets since its 1963 chartering. It had no full-time employees.OGEMA, Wis. – NCUA and state regulators took over and liquidated tiny Wisconsin Heights CU this afternoon and assigned the member accounts of the fourth credit union failure of 2011 to CoVantage CU, the $860 million credit union based in nearby Antigo.

March 4 -

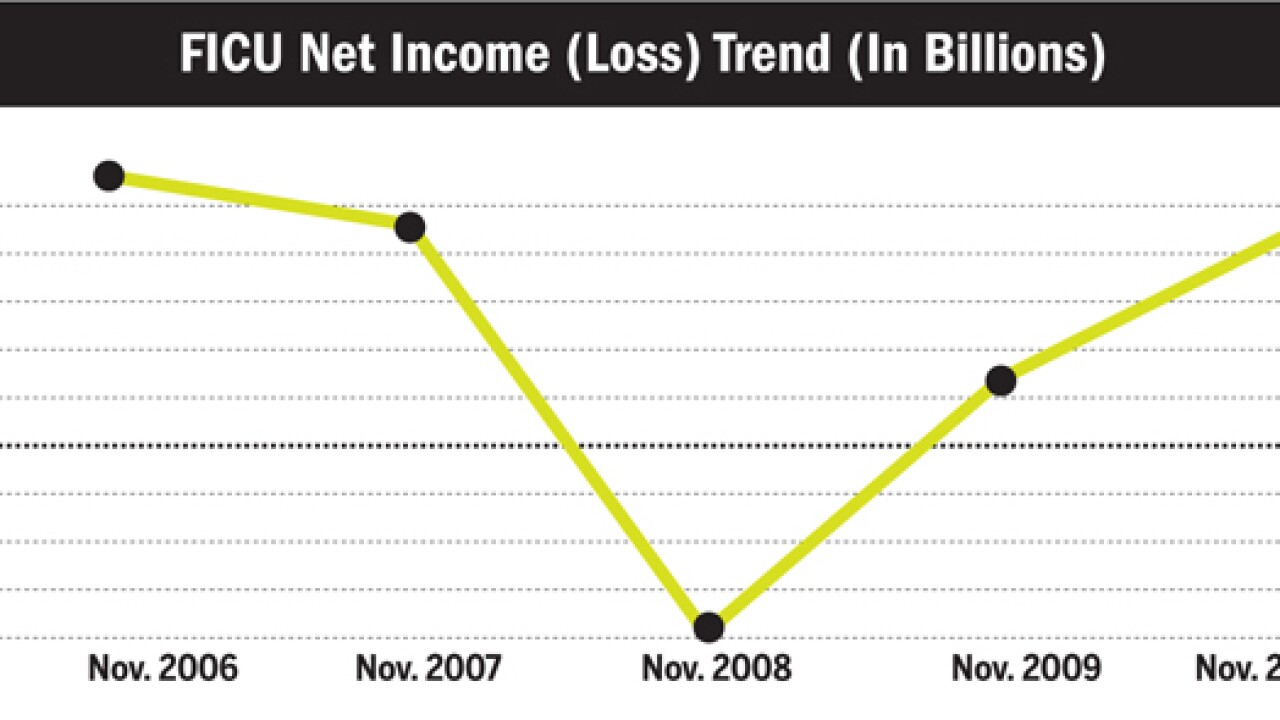

ALEXANDRIA, Va. – Credit unions across the country reported a strong fourth quarter, cutting operating expenses to boost return-on-assets, as the economic rebound appears at hand, according to NCUA. ROA, the key profitability indicator, rose to 0.51% for the fourth quarter, up from 0.45% for the third quarter, and just 0.18% at year-end 2009. While operating expenses -- including stabilization expenses, cost of funds, and provision for loan loss expenses -- declined. Still, there are some troubling signs, as both lending and membership declined in the fourth quarter, while share growth was very tepid, less than 1%. For the year, lending declined by more than 1.3%. “Credit unions, as a whole, are exhibiting positive trends in their operations,” said NCUA Chairman Debbie Matz. “As the nation emerges from a prolonged economic contraction, the stabilization of many strategic indicators and evidence of improving economic trends demonstrate positive developments for credit unions.” “Virtually every key ratio improved by year-end -- net worth climbed to 10.06 %; return on average assets grew 33 basis points after recovering from a decline in 2008 and showing slight improvement in 2009; and delinquencies, charge-offs, and cost of funds declined.” Delinquencies remained at historically high levels, ending 2010 at 1.74%, and the charge-off ratio was 1.1% Credit union member bankruptcies continue to increase also and were up by 3% over 2009 to a new high.ALEXANDRIA, Va. – Credit unions across the country reported a strong fourth quarter, cutting operating expenses to boost return-on-assets, as the economic rebound appears at hand, according to NCUA.

March 3 -

WHEELING, W.Va. — Members of Center Valley FCU, brought down by CEO fraud that drained some $9 million from the institution, continue to pursue an accounting for losses on their share accounts and for missing loan payments, authorities said last week after the former CEO, Bernie Metz, was sentenced to nine years in prison.

February 25 -

ALEXANDRIA, Va. — NCUA reported that during January it did not write off any of the National Credit Union Share Insurance Fund's (NCUSIF) assets as insurance loss expense. NCUA had budgeted for as much as $54.2 million in insurance fund losses during the month.

February 25 -

SANTA ROSA, Calif. – Redwood CU announced today it has agreed to absorb Cal State CU Of North Bay, an ailing one-time $110 million credit union located in the same town. Cal State CU, which reported net worth of just 3.7% and assets of $90 million at year-end, is the second large California credit union to be merged out in recent weeks, following Oakland Municipal CU, a one-time $110 million credit union that was acquired by Western FCU. The deal will give $1.7 billion Redwood, which reported net income of $6.1 million for 2010, four additional branches in its core market.

February 18 -

MADISON, Wis. — CUNA Mutual Group is reporting net income for 2010 of $87-million, a 58% increase over one year earlier, despite a struggling economy and flat to negative growth at most credit unions.

February 11 -

SAN BERNARDINO, Calif. — Arrowhead Credit Union, which was battered by huge losses in 2008 and 2009, managed to cut its 2010 net loss to just $4.4 million.

February 11 -

ALEXANDRIA, Va. – The NCUA Board will follow the banking regulators and propose a rule next week that will give the agency oversight over executive compensation for the largest credit unions, those over $1 billion. The rule to be issued for public comment will bar bonuses and other compensation packages tied to risky activities–such as the ones NCUA alleges helped sink WesCorp FCU–and will require the big credit unions to disclose pay packages for all executive officers. That will include: president, chief executive officer, executive chairman, chief operating officer, chief financial officer, chief investment officer, chief lending officer, chief legal officer, chief risk officer, or head of a major business line. The proposed rule is required under provisions of the Dodd-Frank Financial Reform Act which seeks to rein in excessive Wall Street compensation that was found to be tied, in many cases, to risky activities that caused some of the biggest losses during the financial crisis. The FDIC proposed additional provisions on the biggest banks, those over $50 billion, which would require those firms hold on to at least half the bonuses paid to top executives for three or more years. There are about 175 credit unions over $1 billion in assets that the NCUA will would apply to. The proposed rule is supposed to be effective six months after publication of the final rule in the Federal Register, with annual reports due within 90 days of the end of each institution’s fiscal year. The other agency’s proposing the rule are the Federal Reserve, Office of the Comptroller of the Currency, Office of Thrift Supervision, the Securities and Exchange Commission and Federal Housing Finance Authority, the regulator for Fannie Mae, Freddie Mac and the 12 Federal Home Loan Banks.ALEXANDRIA, Va. – The NCUA Board will follow the banking regulators and propose a rule next week that will give the agency oversight over executive compensation for the largest credit unions, those over $1 billion.

February 10 -

LENEXA, Kan. – CommunityAmerica CU paid its members a bonus dividend for 2010 of $1 million on Tuesday, double last year’s payout.

February 9 -

ALEXANDRIA, Va. – NCUA said this afternoon it is undecided whether it follow the banking agencies’ lead in proposing a new rule prohibiting incentive-based compensation deals that encourage big risk taking by management. The FDIC and the three other banking agencies, the Federal Reserve, Office of the Comptroller of the Currency, Office of Thrift Supervision–all of whom drafted the rule with NCUA–issued the rule for public comment today. The NCUA Board is scheduled to be briefed on the proposal next week. The NCUA proposal would apply to all executive officers of large credit unions, the 175 institutions over $1 billion in assets. The proposed rule defines “executive officer” as a person who holds the title or performs the function of: president, chief executive officer, executive chairman, chief operating officer, chief financial officer, chief investment officer, chief lending officer, chief legal officer, chief risk officer, or head of a major business line. The proposed rule is required under provisions of the Dodd-Frank Financial Reform Act which seeks to rein in excessive Wall Street compensation that was found to be tied, in many cases, to risky activities that caused some of the biggest losses during the financial crisis. The FDIC proposed additional provisions on the biggest banks, those over $50 billion, which would require those firms hold on to at least half the bonuses paid to top executives for three or more years. But credit unions have also been tainted by allegations of risky behavior by bonus-seeking management. NCUA is suing executives of WesCorp FCU over claims the management of the one-time $34 billion corporate engage din risky activities to boost the corporate’s profits and earn big bonuses. The proposed rule is supposed to be effective six months after publication of the final rule in the Federal Register, with annual reports due within 90 days of the end of each covered financial institution’s fiscal year. The other agency’s proposing the rule are the Securities and Exchange Commission and Federal Housing Finance Authority, the regulator for Fannie Mae, Freddie Mac and the 12 Federal Home Loan Banks.

February 7 -

CHICAGO – Alliant CU has landed in new markets with the completion of its acquisition of Continental FCU, the target of the unsuccessful 2007 hostile takeover which eventually cost members of the airline employees credit union a promised $5 million payout. Continental fended off a proposed 2007 takeover by Wings Financial CU in which the Minnesota credit union promised to pay out $5 million of Continental’s excessive capital to members after completion of the bid, which was noted for being the first non-consensual–or hostile-- merger offer among credit unions. But by the time Alliant, the one-time American Airlines employees credit union, completed its deal for Continental, losses had erased almost all of the smaller credit union’s capital and eliminated any chance of a merger dividend. The hostile offer by Wings Financial caused such a controversy in the credit union movement that the one-time Northwest Airlines employees credit union was forced to withdraw its offer and with it the promised $5 million member payout. As a result, Continental members ended up with nothing, with the credit union piling on additional losses since then that wiped out virtually all of its capital. Continental, a one-time $210 million credit union which serves employees of Continental Airlines and U.S. Airways, reported a $9.6 million loss for 2009 and a $9.3 million loss for 2010, as net worth declined to just $561,000 on $150 million in assets. The Continental deal will give $7.6 billion Alliant seven additional branches in Arizona, California, Texas and New Jersey, including facilities at George Bush Intercontinental and Newark International airports, in Houston and Newark, N.J., respectively.

February 7 -

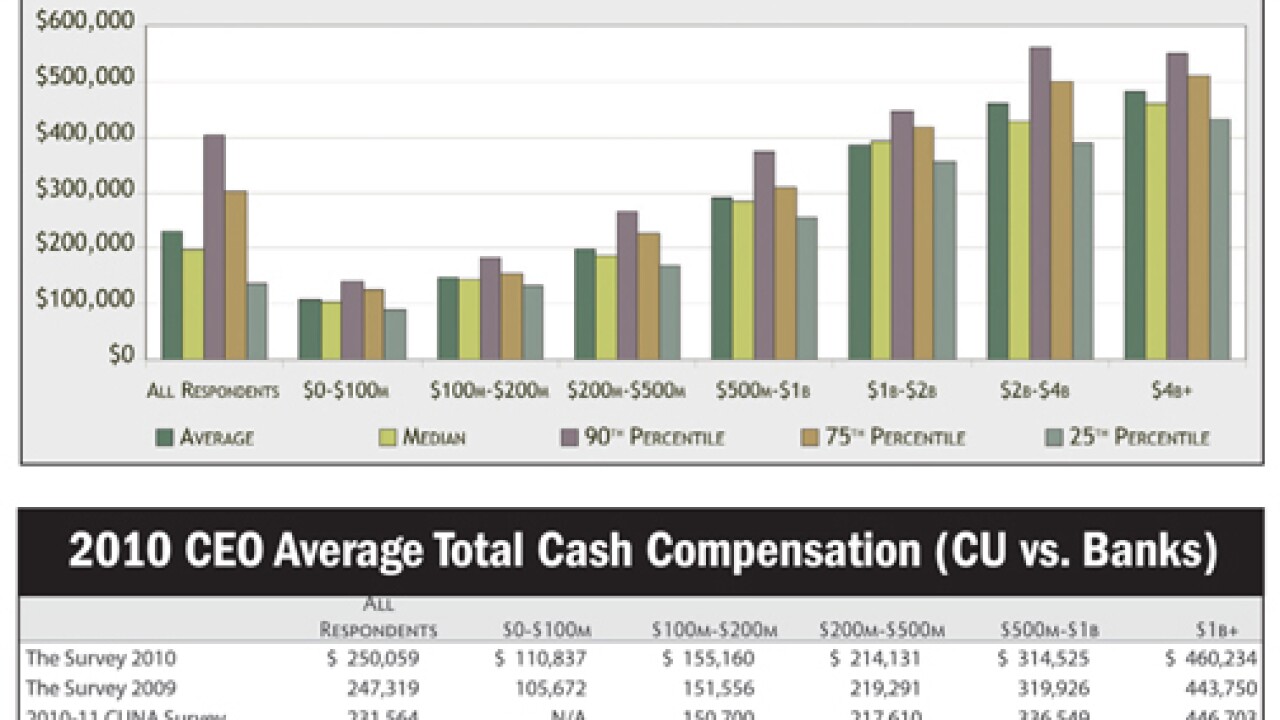

COVINA, Calif.-Credit union CEOs received larger pay increases in 2010 than in 2009, a sign that the CU industry and the economy are recovering, reports Executive Compensation Solutions (ECS).

February 7

-

SAN FRANCISCO – NCUA and state regulators today closed Oakland Municipal CU and assigned the remnants of the one-time $130 million credit union to Western FCU, the $1.5 billion Manhattan Beach-based credit union. Oakland Municipal, the first credit union failure of the year, lost $4.9 million for 2009 and another $900,000 for 2010, and was inadequately capitalized. The credit union was chartered in 1936 by Oakland city employees and expanded to serve all residents of the city and of San Leandro.

February 4 -

SACRAMENTO – The Golden 1 CU, the nation’s sixth largest credit union, became the latest California credit union to erase losses, reporting today it went from a $23.1 million loss in 2009 to $76.1 million net in 2010, not counting a $15.8 million charge for NCUA assessments. The news is further evidence that the state’s credit union crisis is waning, with other California giants also moving from the red to the black in recent days. San Francisco’s Patelco CU went form a $14.6 million 2009 loss to a $24.6 million 2010 net; Kinecta FCU went from a $71.3 million 2009 loss to a $14.6 million 2010 net; Wescom Central CU from a $93.6 million loss to a $2.7 million net; North Island CU from a $52.4 million loss to an $11.4 million net; and Redwood CU from an $11.5 million loss for 2009 to a $6.1 million loss for 2010. Other Golden State credit unions moving from the red to the black last year were: AltaOne CU, and Schools Financial CU. Like the other credit unions, the Golden 1, the state’s second largest credit union, cut provisions for loan and lease losses–the amount moved to its allowance for loan losses for the entire year–by two thirds, from $126.2 million to $42.5 million, a sure signal that bad loans have been squeezed out of its balance sheet.

February 1 -

OREM, Utah – NCUA reported yesterday that continuing loan losses at Family First FCU erased all of the one-time $170 million credit union’s capital last year, leaving it with negative net worth of almost $13 million, the latest big Utah credit union to become insolvent.

January 31 -

SAN FRANCISCO — Mission SF Federal Credit Union says it needs $200,000 over the next two months to keep its doors open, and it is putting out feelers to potential investors.

January 28 -

LOS ANGELES — In a new sign of economic recovery, credit unions are moving tens of millions out of their loan loss reserves, enabling them to reduce red ink, and in some cases, move into the black.

January 28