Kate Berry has covered the Consumer Financial Protection Bureau for American Banker since 2016. She joined the publication in 2006 covering mortgage lending and the financial crisis. Berry also has covered big banks including Bank of America, J.P. Morgan Chase and Wells Fargo. She has won five awards from the Society of American Business Writers and Editors, and has worked at several news organizations including the Orange County Register, the Los Angeles Business Journal and the Associated Press. Berry began her career as a clerk at the New York Times.

-

A loan-mod outreach firm's technology evokes Big Brother; an illiquid-asset auctioneer starts a secondary market for California IOUs; and more.

July 29 -

During the boom, loans were often set up without an escrow account for property taxes and insurance, which traditionally are collected monthly by the servicer along with principal and interest. Leaving taxes and insurance out of the monthly bill made the mortgages look more affordable to borrowers (who often got hit later with a large annual or semiannual tax bill). Today, many of these subprime borrowers are trying to get loan modifications. But servicers generally require that an escrow account be created as a condition of rewriting loan terms. This is one reason that so many borrowers who get modifications redefault, observers said.

July 27 -

Freddie Mac is bringing in reinforcements to speed up the loan modification process.

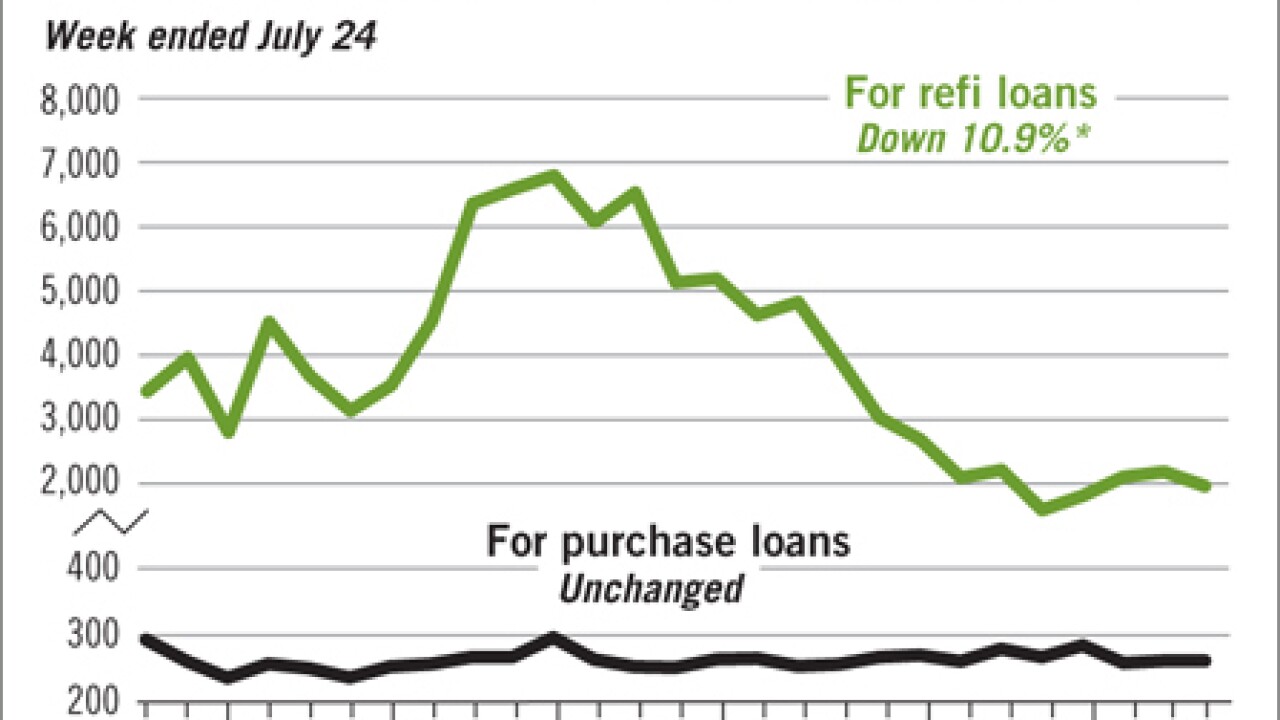

July 24 -

When comparing the loan modification efforts of the top mortgage servicers, it's hard to find rhyme or reason behind their decisions, observers say.

July 23 -

-