Consumer banking

Consumer banking

-

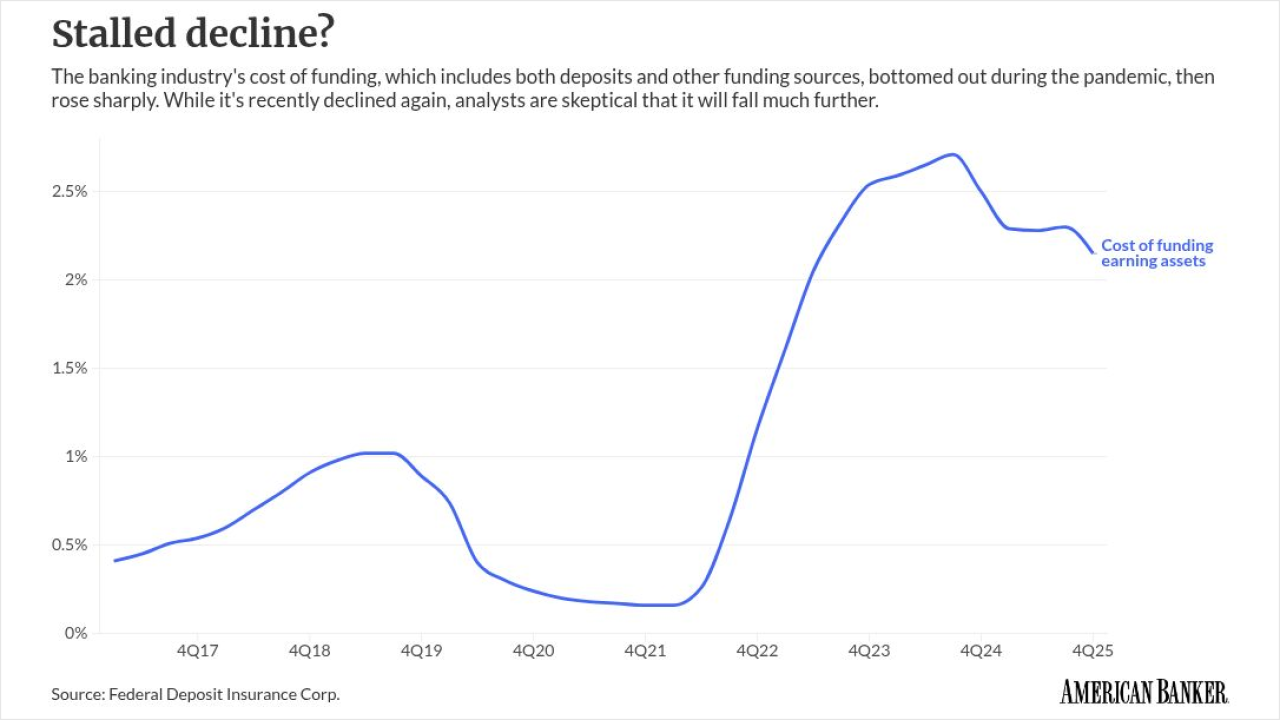

Banks' deposit costs fell as the Fed made borrowing cheaper. But signs of increased competition are already emerging, and analysts see a tougher road ahead.

1h ago -

Stephan Feldgoise and Joshua Schiffrin will join Goldman Sachs' management committee; Fidelity Investments is dismissing about 800 personnel as it restructures its technology and product-delivery teams; Citi has hired JPMorgan's André Ross as its country officer and banking head for South Africa; and more in this week's banking news roundup.

May 8 -

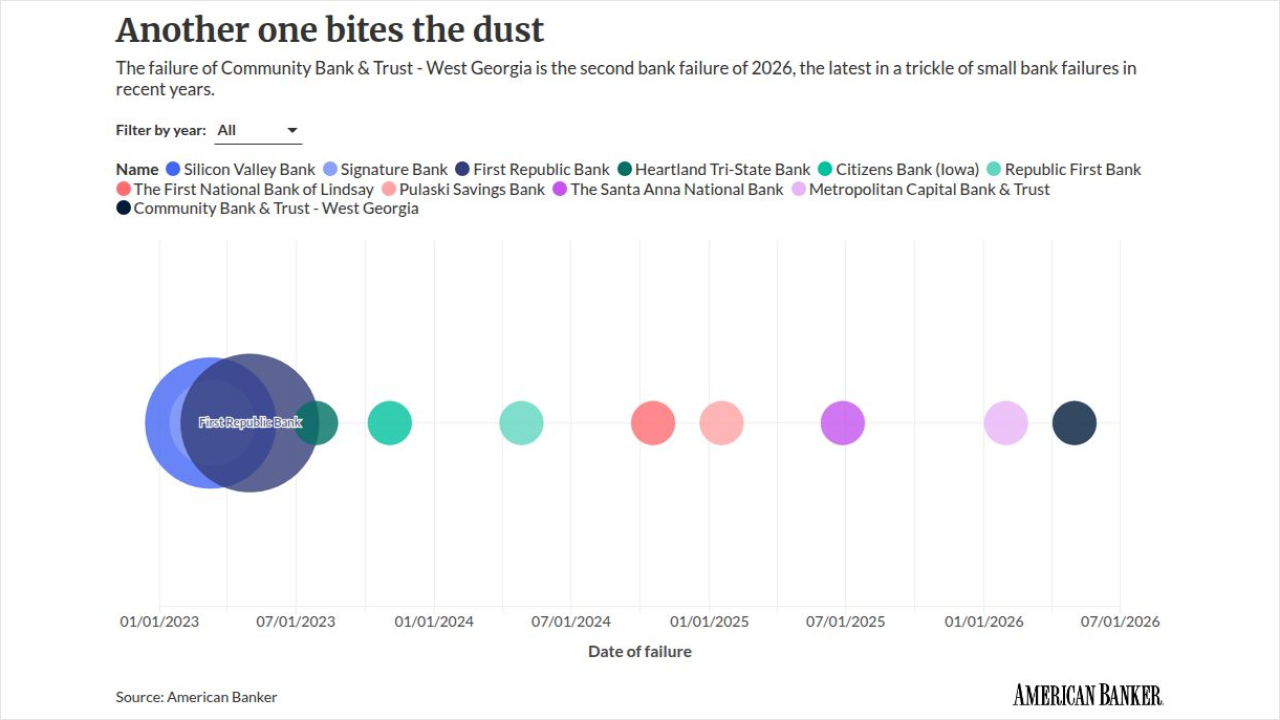

Almost 60 SBA loans originated by Community Bank & Trust — West Georgia were classified as noncurrent, according to Small Business Administration records. Last week, Community became the second U.S. bank to fail in 2026.

May 8 -

An April 20 bankruptcy filing accuses Kfir Gavrieli of recruiting friends, family and his synagogue to sign sham contracts that inflated Aspiration's revenue.

May 7 -

The megabank's first investor day in four years offered a comprehensive look at how it plans to grow profits and drive higher returns in the coming years. Part of the strategy involves branch updates.

May 7 -

The newly opened bank founded by big tech executives reached the deposit milestone within its first quarter of operations, according to a recent call report.

May 6 -

On Thursday, Citi will hold its first investor day in four years. The megabank, which has undergone substantial change under CEO Jane Fraser, is expected to share its strategy for driving higher profitability, deploying AI and ramping up shareholder returns.

May 6 -

Public comments on the Office of the Comptroller of the Currency's GENIUS Act implementing regulations highlighted the rift between banks and crypto firms over the permissibility of yield on stablecoin holdings, an issue that has stalled crypto market structure legislation for months.

May 6 -

Opportunity favors the prepared, and Cambridge Savings Bank had been saving for years to buy a nearby rival. Now, as the mutual bank announces plans to acquire First Seacoast Bank, it says it's found "the right deal at the right time."

May 5 -

Carter Bankshares wants to widen its footprint in the Carolinas and may look to buy a bank, especially in South Carolina, where it set up a loan production office in November. The Virginia bank recently resolved a long-running dispute with a major commercial borrower.

May 5 -

Two U.S. banks have failed so far in 2026, continuing the recent pattern of smaller lenders collapsing abruptly due to firm-specific issues. January's failure of Metropolitan Capital Bank & Trust and the early May failure of Community Bank & Trust – West Georgia both fit that mold.

May 4 -

Community Bank & Trust in Georgia, the second bank failure this year, shows what happens when bankers don't keep things simple.

May 4 -

The FDIC moved quickly on Friday to sell $288 million in assets Community Bank and Trust – West Georgia to Anchor Bank, but the sale announcement leaves the fate of $27 million in uninsured deposits to be determined.

May 1 -

Banner Bank is poised to merge with Bank of the Pacific in an all-stock deal valued at $177 million. The two Washington-based commercial banks both have branches in Washington and Oregon.

May 1 -

BayFirst Financial in St. Petersburg named veteran Tampa-area banker Al Rogers as its CEO and announced an $80 million capital raise. The bank sold its SBA-lending business last year, but it's still struggling to work through problems in its legacy loan portfolio.

May 1 -

Miami's Ocean Bank appointed Yuni Navarro to its board of directors; Indiana-based Interra Credit Union announced it will acquire The Hicksville Bank in Ohio; JPMorganChase hired Chris Mihok from Keefe Bruyette and Woods; and more in this week's banking news roundup.

May 1 -

The Japan-linked risk for banks is not the exchange rate itself but the funding, collateral and rollover pressure behind it. Sudden volatility in the foreign exchange market will rapidly cascade into U.S. Treasury markets.

April 30 -

The Spanish banking giant is seeing improvement in its U.S. business, which is set to expand significantly if its pending acquisition of Webster Financial gets approved.

April 29 -

Community banks' primary objection to the Main Street Depositor Protection Act appears to be that one provision of it would give credit union customers the same level of deposit protection as bank customers.

April 29 -

Banks have a narrow window to shape how agent identity verification works before transaction volumes force ad hoc approaches that will be harder to standardize later.

April 29