-

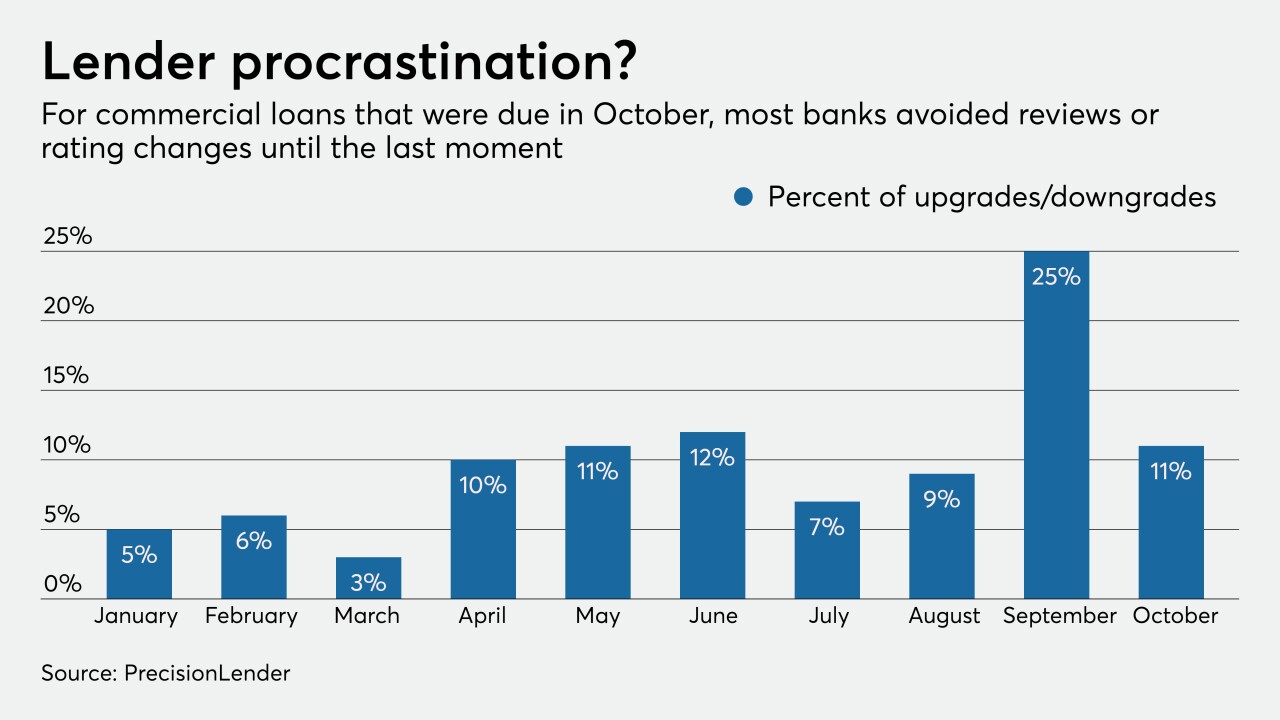

Some lenders are poring over commercial portfolios more frequently than normal — perhaps as often as once a month — to uncover problems hidden by payment deferrals and government stimulus before it's too late.

December 8

December 8

-

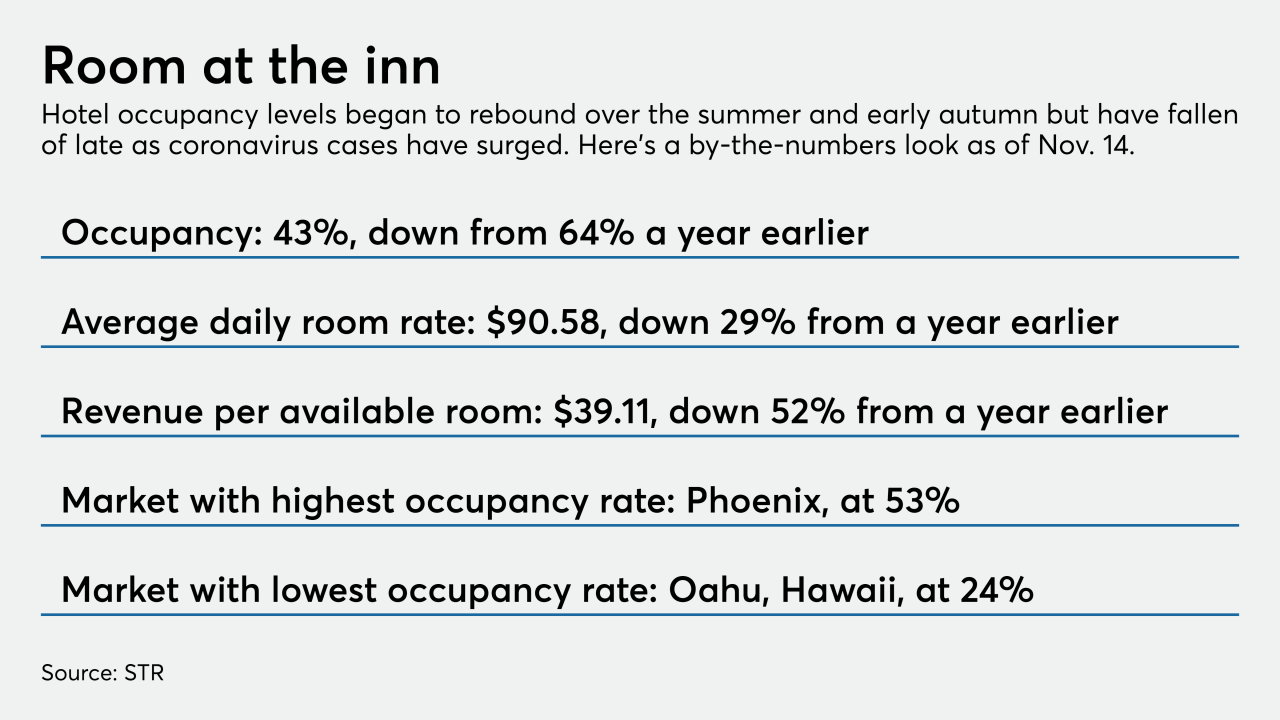

Hospitality sector credits are coming out of forbearance just as coronavirus cases surge. Restructurings and charge-offs could mount unless vaccine distribution happens quickly enough to jump-start travel by mid-2021.

November 23

-

The Ohio company will benefit after settling unpaid judgments tied to nonperforming loans at a bank it bought before the last financial crisis.

November 19 -

Lending opportunities have become scarce, especially with commercial borrowers, and banks are resisting the temptation to relax standards to boost volume.

November 12

-

The region now leads the nation in virus cases, and with winter lurking the fear is that the outbreak will only get worse.

November 5

-

A prosperous decade leading up to the pandemic had left lenders in good shape, but they're worried the economic shock to the state's most vital industry could linger into 2022.

November 2

-

The New Jersey company reported a quarterly loss after becoming one of the first lenders to liquidate loans harmed by the coronavirus pandemic.

October 30

-

Lenders pushed back against the notion that city dwellers' pandemic-driven flight to suburbia would hurt them. They say fewer landlords have sought deferrals as vacancy rates remain low and rent collections have stabilized.

October 29

-

The subprime lender cited low odds that Washington will deliver further economic relief, and the fact that $1.5 billion of loans whose deferral period expired are now more than 30 days behind.

October 28

-

The company's Silicon Valley Bank unit reduced its loan-loss cushion by $52 million. Private-equity and VC clients have warmed to the practice of doing deals virtually, which increases lending opportunities, SVB executives said.

October 23

-

The Cincinnati company, one of just a handful of lenders to reduce its cushion against bad credits in the third quarter, was grilled by analysts who suggested it was being too optimistic about the long-term effects of the pandemic recession.

October 22

October 22

-

Banks have managed to steer around trouble spots in energy, hotel and mall-related credits. But fears of further deterioration, an eviction wave or more job losses are keeping lenders circumspect.

October 21

-

Weak loan demand, persistently low yields and the continued struggles of sectors such as hospitality and retail are among the myriad lending challenges facing small regional banks.

October 20

-

Spending is up and deferrals are down sharply, signaling that the economy has turned a corner, CEO Brian Moynihan said. The outlook stood in stark contrast to JPMorgan Chase, which set aside more funds to address potential exposure in consumer banking.

October 14

-

The banking giant may be sitting pretty with plenty of money reserved for bad loans — or it could have to set aside billions more in coming quarters. It hinges on an ongoing U.S. recovery and the passage of a new stimulus package.

October 13

-

The company defied expectations by cutting its reserve for loan losses by $569 million, after adding $20 billion to the allowance in the first half.

October 13

-

Deferrals may be hiding credit issues, leading lenders to track deposit flows, property maintenance and other factors to gauge the true health of their portfolios.

October 8

-

Low rates and intense competition might lead some banks to ease underwriting standards in 2021, when the economy may not yet have recovered.

October 5

-

Commercial real estate loans are vulnerable as financial assistance for tenants winds down and might not be fully renewed. Late rent payments could rise, leading lenders to press landlords to pay up.

September 23

-

Originations in the third quarter are on pace to double what the Detroit lender reported a quarter earlier, adding more high-yielding loans to the balance sheet.

September 15

September 15