-

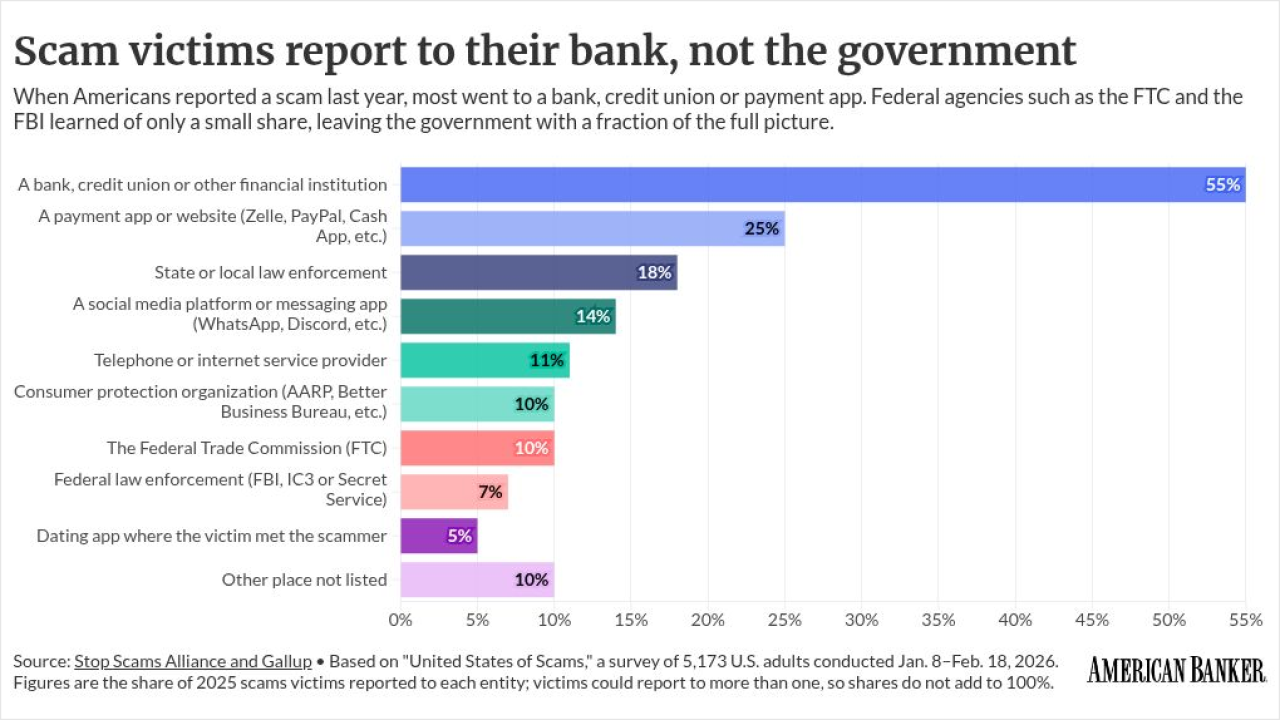

Only 13% of scams reach federal agencies. The rest land at banks and payment apps, making them the country's de facto scam-reporting system.

July 22

July 22

-

The Denver-based bank reported that two loans soured, one due to fraud. A number of other lenders reported sizable fraud-related losses last fall.

July 10

July 10

-

The largest crypto theft of 2026 hit Drift Protocol after attackers exploited a small security council, putting a spotlight on DeFi vulnerabilities.

April 2

-

Dallas Turner, a linebacker for the Minnesota Vikings, sent $240,000 via wire transfers after scammers convinced him someone was impersonating him.

July 14

-

Listen to Gasan Awad, SVP, Fraud Director, Enterprise Fraud Product Management at PNC Bank, Chris Briggs, Chief Product Officer at Mitek and Jay Leal, CIO at Vantage Bank.

-

Texas' SB 1281 introduces harsher penalties — up to life in prison — and targets check fraud as banks report rising financial crimes tied to stolen mail.

June 27

-

Early Warning, which operates the payment network, says the rate of reported fraud is less than a tenth of one percent. Yet stories of consumers who have fallen victim to scams and lost money as a result abound.

May 28

May 28

-

Preliminary rulings by a Pennsylvania judge will allow a jewelry company that claimed it lost $1.1 million to fraud to move forward with suing individual bank employees.

March 26

-

Wars in Ukraine and the Middle East. Fiercely polarized U.S. politics. Rapidly multiplying payments options on social media networks and elsewhere. Those factors and more are making it harder than ever for banks to combat illicit financial transactions.

March 25

March 25

-

A study from Surfshark found that crypto scams cost their victims about five times as much money as losses from other cybercrimes.

June 7 -

Fraudsters continue to impersonate owners of small and midsize businesses at a rate comparable to the early days of the pandemic. Many lenders can take simple steps to mitigate it.

May 3

-

The plaintiffs allege that the banks did not catch obvious red flags or implement proper safeguards such as requiring two employees to approve each transaction.

January 6

-

Although the number of scam attempts is falling, especially in financial services, costs are up, data shows.

May 4

-

Chicago Title Insurance Co. and Chicago Title Co. LLC agreed to the payment to resolve a lawsuit brought by the bank, which said the firms had helped orchestrate a borrowing scam involving liquor licenses, according to a regulatory filing.

March 8 -

The “new normal” of COVID-19-influenced retail is actively being exploited by fraudsters, as LexisNexis Risk Solutions finds fraud costs for U.S. retailers rising in 2020 by 7.3% over last year’s data.

July 21

July 21

-

A 2019 report from the Federal Trade Commission shows consumer losses to “romance scams” rose more than 300% between 2015 and 2018. Credit union leaders say the real numbers may be much worse.

February 14

February 14

-

Two former officials were sentenced to five years each for falsifying travel expenses and lying to authorities.

December 23

December 23

-

Prosecutors allege that Sylvia Ash, a judge in Brooklyn, N.Y., helped Kam Wong, the former CEO of Municipal, cover up his fraud scheme.

October 16

-

Though synthetic identity fraud is down across the industry, there's been an uptick in such attacks targeting credit unions.

October 8

-

Recent reports that counterfeit card fraud is markedly down in the U.S. since the introduction of EMV chip cards in 2015 is fantastic news, except for retailers that also sell goods sells online. In that case fraud has merely moved from an in-store payment attempt to a card not present (CNP) one. For e-commerce only stores the rise in payments fraud attempts has been a deluge.

October 2