While overall payments declined, the financial sector remained the top payer to cybercriminals, surpassing both health care and manufacturing.

Birthday greetings from Facebook friends are far more dangerous than many consumers realize.

-

As the toll of financial crime rises, the card network is attempting to boost its fraud-fighting game by buying threat intelligence firm Recorded Future.

-

The card network is building a model for account-to-account payments, which are gaining popularity, while Swedish regulators criticize Klarna's money-laundering prevention efforts. That and more in American Banker's global payments roundup.

-

As the Consumer Financial Protection Bureau increases scrutiny of earned wage access, cash-back fees and airline rewards, industry lobbyists are pushing back, while some groups cheer the move.

A near-collapse of the global software vulnerability database exposed critical weaknesses that could leave banks unable to track cyber threats.

-

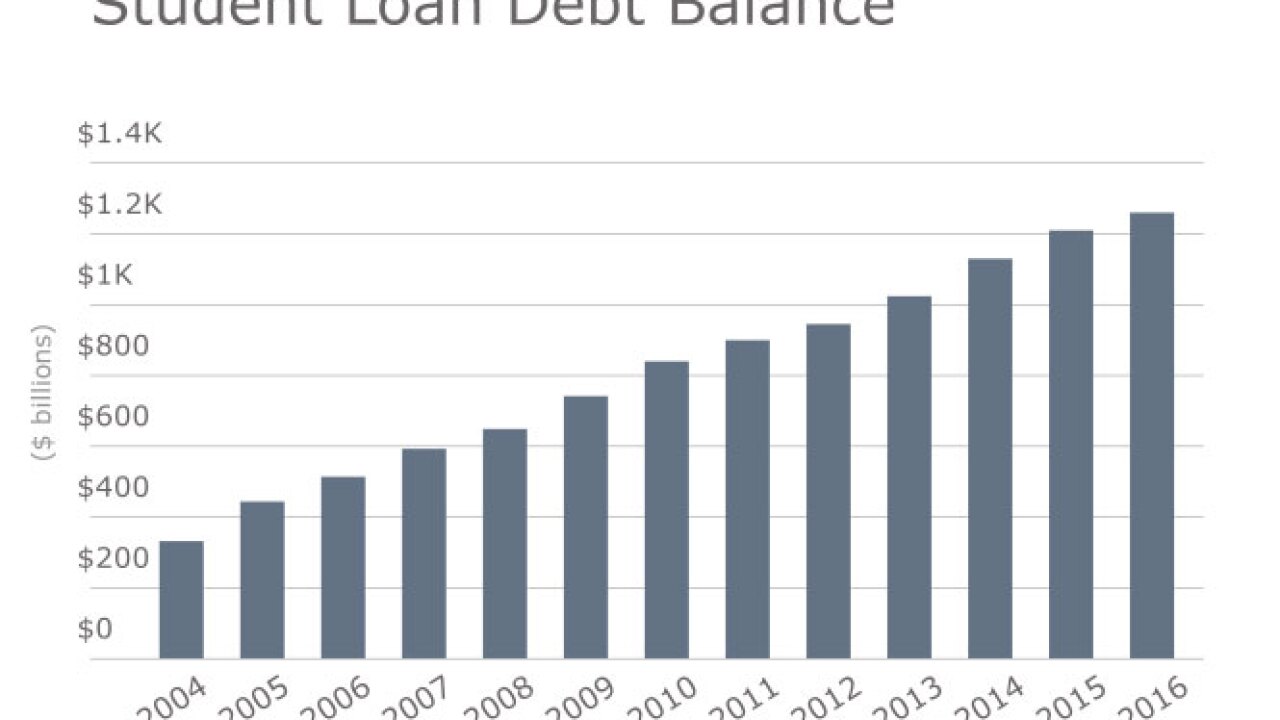

Fintech firms and millennial-focused advisers are providing advice on student loan refinancing, with the expectation that over time it will eventually lead to new business, in the form of brokerage and retirement accounts.

-

A handful of banks and fintech companies are letting bank customers connect via chat bots on platforms like Slack of Facebook messenger. Some say this is the next big thing, while others say the technology still has a ways to go.

-

Changes in consumer behavior including a growing distrust of financial advisers are driving the rise of robo advisers, says Gauthier Vincent, a consultant with Deloitte.

-

Federal backing for firms facing a deluge of missed mortgage payments is still on the table despite recent comments by an official who questioned the need to help the industry.

-

Wells Fargo tells business clients to consider other banks for emergency loans; JPMorgan Chase is temporarily reducing its exposure to the mortgage market; how TD Bank got a head start on pandemic preparations; and more from this week's most-read stories.

-

Stress and exhaustion are catching up to lenders and call center employees helping customers grapple with the coronavirus pandemic.

The Sandy, Utah-based credit union opted to part with its two New Mexico branches to focus on other geographies. At least one expert expects an uptick in branch sales as more credit unions seek to "right-size" their networks.

Questions remain whether Trump can legitimately remove board members from the National Credit Union Administration, and the answers lie in the courts.

-

The secretive world of private credit is increasingly being funded by public money, and there will be no FDIC there to bail us out when things go bad.

-

Any comprehensive overhaul of the Federal Home Loan Bank System will have to navigate a dense thicket of countervailing regulatory and stakeholder priorities.

-

Republican Josh Hawley, the senior senator from Missouri, says he intends to offer legislation that would cap credit card rates at 18%. For a bill designed to go nowhere, it's a surprisingly good idea.

-

Treasury Secretary Scott Bessent said the Federal Reserve Board should reject the renomination of any regional Federal Reserve Bank presidents who have not lived in their districts for three years, signaling a potential confrontation when reappointments come before the board in February.

-

In a sternly worded letter, Sen. Elizabeth Warren and Rep. Maxine Waters demanded to know why federal agencies haven't provided more guidance since the one-cent coin was discontinued. They accused the Trump administration of making an "abrupt and unilateral decision" without thinking it through.

-

Royal Bank of Canada now expects to achieve an annual return on equity of at least 17% by 2027, executives said Wednesday, up one percentage point from the bank's earlier goal.

-

Companies such as Google, Visa and Mastercard are building a framework that will allow AI agents to shop and make payments. There are signs that consumers are warming to the idea.

-

The Toronto-based loan fintech received an IFE license from Puerto Rico to launch Propel Bank.

-

As federal watchdogs step back from regulating "Buy Now, Pay Later" loans, state authorities are stepping in. This week, the attorneys general from California and several other blue states joined the fight.

- Daily BriefingDelivered Every WeekdayIdeas that impact your business delivered to your inbox every day.

- TechnologyWednesday, ThursdayThe latest industry developments from digital banking to cybersecurity to AI.

- PaymentsDelivered Every WeekdayAn early-morning roundup of important headlines from the past 24 hours.

- Best of the WeekFridayThe most important and widely read stories from the previous week.

The Consumer Financial Protection Bureau said the new oath was necessary because prior leadership engaged in what it describes as "thuggery" during exams. Former CFPB officials rejected the agency's characterization of past actions.

Regulators officially ended the high-profile enforcement action over the 2020 breach, a move applauded by security leaders fearing personal liability.

The 23rd annual ranking of women leaders in the banking industry.

-

Sponsored by Talkdesk

Sponsored by Talkdesk -

Sponsored by IntraFi

Sponsored by IntraFi -

Sponsor Content from Equifax

Sponsor Content from Equifax -

Sponsor Content from Equifax

Sponsor Content from Equifax